Why It's Reasonable to Be Bullish Stocks and Gold / Commodities / Gold and Silver 2021

Another day, another reversal – and a positive one forstocks. Universal sectoral weakness gave way to a unison rebound amidconstructive outside markets. After weeks of on and off fits over rising Treasuryyields, S&P 500 ran into headwinds on their retreat, and recaptured itsluster yesterday as long-dated Treasuries (TLT ETF) rolled over to thedownside. I guess nothing boosts confidence as much a troubled 7-year Treasuryauction.

While it‘s far from full steam ahead, it‘s a welcomesight that the reflation trade dynamic has returned, and that technology isn‘t standing in the way. I think we‘re onthe doorstep of another upswing establishing itself, which would be apparentlatest Monday. Credit markets support such a conclusion, and so does thepremarket turn higher in commodities – yes, I am referring also to yesterday‘srenewed uptick in inflation expectation.

Neither running out of control, nor declaring theinflation scare (as some might term it but not me, for I view the markets as transitioning to a higher inflationenvironment) as over, inflation isn‘t yet strong enough to break thebull run, where both stocks and commodities benefit. It isn‘t yet forcing theFed‘s hand enough, but look for it to change – we got a slight preview in therecent emergency support withdrawal and taper entertainment talking points,however distant from today‘s situation.

Now, look for the fresh money avalanche,activist fiscal and moterary policy to hit the markets as a tidal wave. Modernmonetary theorists‘ dream come true. Unlike during the Great Recession, the newlyminted money isn‘t going to go towards repairing banks‘ balance sheets – it‘sgoing into the financial markets, lifting up asset prices, and over to the realeconomy. So far, it‘s only PPI that‘s showing signs of inflation in the pipeline– soon to be manifest according to the CPI methodology as well.

Any deflation scare in such anenvironment stands low prospects of success.

That concerns precious metals – neither rising, norfalling, regardless of the miners‘ message. After the upswing off the Mar 08lows faltered, the bears had quite a few chances to ambush this week, yet madeno progress. And the longer such inaction draws on, the more it is indicativeof the opposite outcome.

Yes, that‘s true regardless of the dollar continuing downfor almost a month since my early Feb call beforeturning higher. When I was asked recently over Twitter myopionion on the greenback, I replied that its short-term outlook is bullish now– while I think the world reserve currency would get on the defensive and reachnew lows this year still, it could take more than a few weeks for it to form alocal top. Once AUD/USD turns higher, that could be among its first signs.

Regarding gold, yesterday‘s words are truealso today:

(…) Gold is again a few bucks above its volume profile$1,720 support zone, and miners aren‘t painting a bullish picture. Resilientwhen faced with the commodities selloff, but weak when it comes to retreatingnominal yields. The king of metals looks mixed, but the risks to the downsideseem greater than those of catching a solid bid.

That doesn‘t mean a steep selloff in a short amount oftime just ahead – rather continuation of choppy trading with bursts of sellinghere and there.

What could change my mind? Decoupling from rising TLTyields returning – in the form of gold convincingly rising when yields movedown.

Let‘s move right into the charts (all courtesy of www.stockcharts.com).

S&P 500 Outlook

Yesterday‘s reversal was overall credible – more so inits internals than as regards the daily volume. On a positive and contrarian note, theput to call ratio reached higher highs yesterday, leaving ample room to power aswift upswing should it come to that. And it could as quite many investors arepositioned for a downswing in stocks.

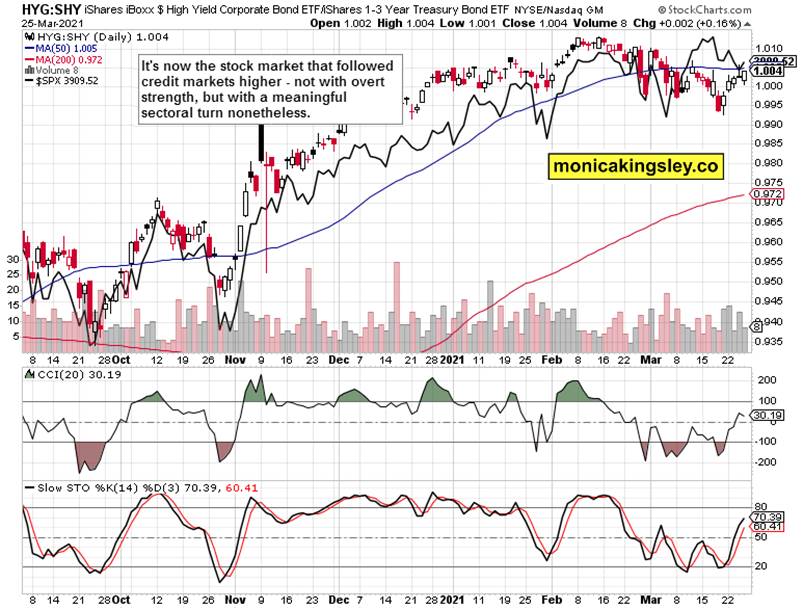

Credit Markets

The high yield corporate bonds to short-dated Treasuries(HYG:SHY) ratio gave up all of yesterday‘s gains, but isn‘t leaving stocks asextended here. Much depends upon whether squaring the risk-on bets wouldcontinue, or not. Both stocks and the ratio appear consolidating here, and notrolling over to the downside.

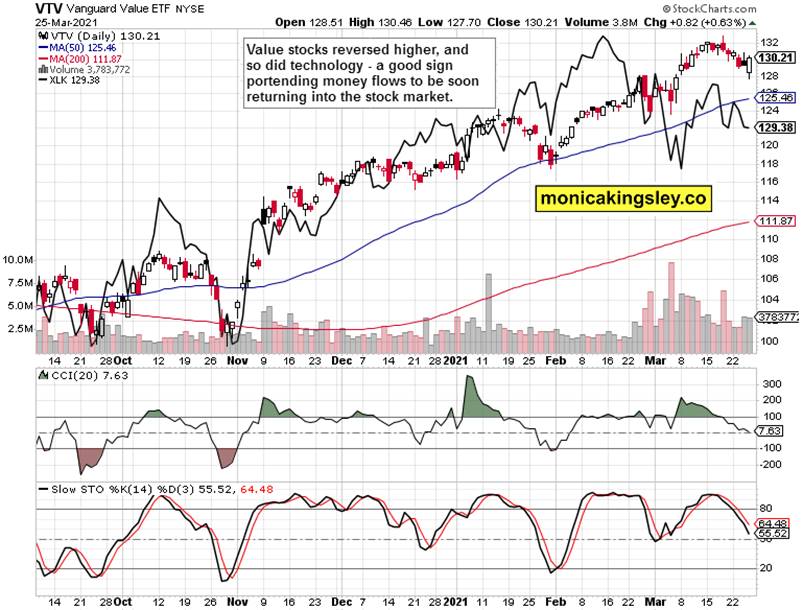

Value and Technology

Value stocks (VTV ETF) finally showed clear leadershipyesterday, the volume didn‘t disappoint, and technology (XLK ETF) recoveredfrom prior downside on top. Closing about unchanged, it‘s key to the S&P500 upswing continuation with force as opposed to muddling through.

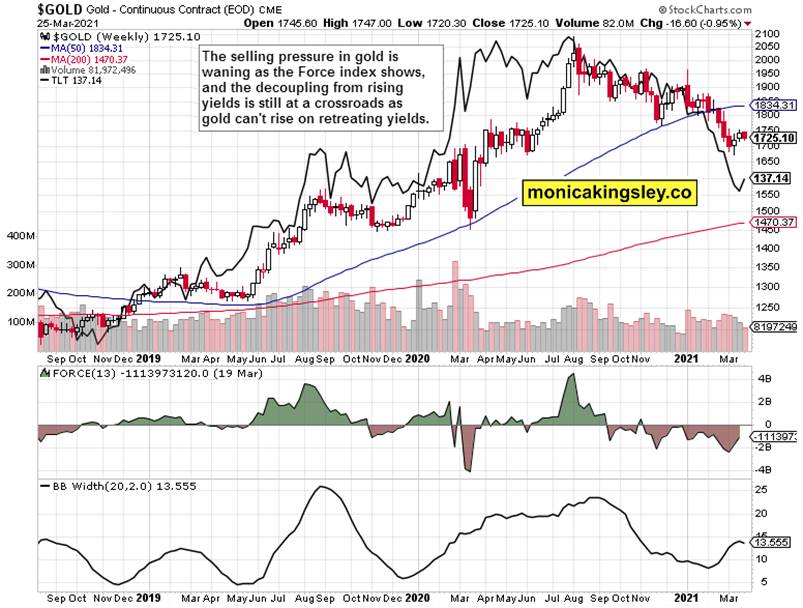

Gold in the Spotlight

The troubled miners got a little less problematicyesterday. The GDX ETF recovered from intraday losses while gold didn‘t exactlyplunge. Its opening strength was a pleasant sight as more often than not,miners‘ weakness while gold goes nowhere, is a signal for going short themetal. But as this sign didn‘t result in a gold slide, my viewpoint is turningbullish again because we might be seeing fake miners weakness that would beresolved over the coming week with an upswing. Now that the Wall and MainStreet expectation for the coming week aren‘t probably as bullish as for theweek almost over, an upswing would be easier to pull off (should it come tothat).

Big picture view remains (positively) mixed – the sellingpressure is retreating but gold isn‘t yet reacting to declining yields. Once itclearly does, the waiting for a precious metals upswing would be over.

Silver and Miners

Silver staged an intraday reversal, which copper couldn‘tpull off. Not that it attempted to, but still the commodities selloff appears abit overdone, given that nothing has fundamentally changed. Both gold andsilver miners stabilized on the day, meaning that the sector is in a wait andsee mode, unwilling to turn bearish just yet.

Summary

The odds of an S&P 500 upswing have gone up, andvolatility made a powerful retreat below 20 once again. Value stocks haveturned upwards, and the stock bulls appear readying another run.

Miners closed at least undecided yesterday, but gold andsilver miners showing outperformance again is missing. Both metals still remainvulnerable to short-term downside. Once goldstrengthens on declining yields, that would be another missing ingredient inthe precious metals bull market.

Thank you for having read today‘s free analysis, which isavailable in full at my homesite. There, you can subscribe to the free Monica‘s Insider Club, whichfeatures real-time trade calls and intraday updates for both Stock TradingSignals and Gold Trading Signals.

Thank you,

MonicaKingsley

Stock Trading Signals

Gold Trading Signals

www.monicakingsley.co

mk@monicakingsley.co

* * * * *

All essays, research andinformation represent analyses and opinions of Monica Kingsley that are basedon available and latest data. Despite careful research and best efforts, it mayprove wrong and be subject to change with or without notice. Monica Kingsleydoes not guarantee the accuracy or thoroughness of the data or informationreported. Her content serves educational purposes and should not be relied uponas advice or construed as providing recommendations of any kind. Futures,stocks and options are financial instruments not suitable for every investor.Please be advised that you invest at your own risk. Monica Kingsley is not aRegistered Securities Advisor. By reading her writings, you agree that she willnot be held responsible or liable for any decisions you make. Investing,trading and speculating in financial markets may involve high risk of loss.Monica Kingsley may have a short or long position in any securities, includingthose mentioned in her writings, and may make additional purchases and/or salesof those securities without notice.

© 2005-2019 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.