Gold Miners Junior Stcks Buying Spree / Commodities / Gold and Silver Stocks 2020

Canadians, at least thosefortunate enough to enjoy a long weekend, returned to their desks Tuesdayto watch gold prices crack another milestone - $2,000 per ounce - as thespectacular summer rally for the precious metal continues.

At time of writing, spotgold’s last bid was $2,019.20, marking a $42 gain since Monday’s tradingsession. Silver prices also experienced a major leg up, with spot silverposting a $1.68 increase to $26.01, as of 17:05 Eastern time - a 7-yearhigh.

The usual suspects arebehind the surges of both metals, ie., worrisome covid-19 infections,geopolitical concerns especially US-China tensions over trade (President Trump tried to forceChina-owned TikTok into selling its US operations), the South China Sea, fearsof inflation on the back of unlimited monetary stimulus and low interest ratesworldwide.

Bullion prices haveclimbed more than 30% year to date, as investors choose gold as a safe havenamid widespread economic uncertainty created by the pandemic. They believe goldwill hold its value better than other assets such as stocks and bonds.

US economic carnage

Central bank stimulus inthe US has pushed sovereign bond yields to record lows, making gold anattractive alternative, despite offering no interest or dividend income. On TuesdayUS Treasury yields fell, as investors remained pessimistic about the U.S.economy’s health and eyed the slow pace of negotiations in Congress on another[$1 trillion] fiscal relief package to combat the coronavirus pandemic, Marketwatch reported.

Second-quarter US GDPcontracted nearly 33%, its sharpest drop on record, showing the US economy isin its worst recession since the Great Depression. Any near-term recovery nowseems hopelessly optimistic.

The yield on thebenchmark 10-year note slipped 4.8 basis points to 0.514%, its lowest since the“flash-crash” of March 9. That puts “real yields” on the 10-year in negativeterritory, always a bullish signal for gold.

The US government andpolicymakers around the world have no choice but to unleash massive stimulusprograms to help their citizenries to deal with the worst economic downturnsince the 1930s.

According to Bank of America, via Zero Hedge, the amount of global fiscal and monetary stimulus in June hadreached an astronomical US$18.4 trillion in 2020, consisting of $10.4 trillionin government spending and $7.9 trillion in central bank asset purchases, “fora grand total of 20.8% of global GDP.”

The IMF predicts thepercentage of global public debt to rise from 69% of national income last yearto 85% in 2020.

Racking up so much of itsown debt means the United States has to keep interest rates low, to preventonerous borrowing costs.

The country’s publicsector deficit is set to nearly triple, while public debt will rise to 107% ofGDP, according to the IMF.

“The U.S. is being themost aggressive with easing and government spending and as a result we expectto see the biggest deterioration in public finances there,” The Financial Post quotes Mathieu Savary, astrategist at BCA Research.

As an example ofexplosive monetary stimulus via money printing, consider: at the end of 2019,the Fed’s balance sheet as a percentage of GDP was 19%; six months into 2020,it had doubled, to 39%.

Amid the growing pile ofdebt, Fitch on Friday revised its US outlook to negative, “to reflect theongoing deterioration in the U.S. public finances and the absence of a crediblefiscal consolidation plan,” while affirming the country’s AAA rating.

Meanwhile the dollar hasweakened considerably, making bullion cheaper for buyers holding othercurrencies, thus boosting investment demand.

The buck’s retreat isdirectly correlated to America’s failure to control the virus. Cases are stillgrowing daily although at a slower rate than in Brazil and India. The US isapproaching 5 million cases and has over 160,000 covid-19 deaths.

According to HorizonsETFs portfolio manager Nick Piquard, global debt and unlimited money printingare denting confidence in the US dollar as the reserve currency - a subject wehave written on extensively.

“The U.S. dollar systemhas worked so far. But we're getting to the point where there's so much debt inthe world and with this new crisis, there’s even more debt,” Piquard explained to Kitco:

“People arefiguring out that maybe they will have to make some changes to how the U.S.dollar acts as a reserve system. The U.S. is probably going to have to print alot of dollars to bail out all this debt. That’s really fuelling the goldrally.”

“Investors areseeing that this COVID crisis isn't going to go away anytime soon. The caseskeep going up globally. And the longer it takes, the more debt needs to becreated,” Piquard said. “Congress is debating right now about how manytrillions of dollars they're going to have to spend for a new stimulus afterhaving already spent trillions of dollars.”

And even once theCOVID crisis is behind us, the economy is going to be weak for a while, Piquardpointed out.

“After all that moneyhas been spent, it's not like you're going to be able to raise taxes to getthat money back, or it's not going to be easy to raise rates,” he said. “Themarket is anticipating that the Fed is going to have to do more. And all thosethings are just beneficial for gold.”

Gold stocks: adiamond in the rough

Considering all of theabove, it’s no surprise that the only companies in North American stock marketsdoing well right now, the only ones making any money, are those benefiting fromthe pandemic, ie., Big Tech FANGS like Facebook, Google and Apple, and goldstocks.

High gold and shareprices mean it’s time for the gold sector to look at another round of consolidations,which could mean serious gains for smart investors who know where to placetheir share buy orders. A recent report from Sprott Asset Management explains:

While most ofcorporate America is struggling, the gold mining sector is financially robust.Free cash flow generation is more common than not for gold producers, balancesheets are strengthening and dividends are increasing. The current world mininginfrastructure could not be replicated at anything close to historical bookvalue. Therefore, the appetite and financial capacity is low for large scalecapital expenditures that would significantly increase global mining output.While most mainstream companies that populate the S&P 500 Index face a subpar earnings outlook, mining companies look forward to rising earnings andfavorable year-over-year earnings comparisons.

Among the seniorproducers with cash positions above $1 billion at the end of the first quarter,were Agnico Eagle Mines, Kinross Gold and AngloGold Ashanti.

Preliminary Q2 resultsfrom Newmont Goldcorp, Barrick, Yamana and Agnico Eagle show profitable secondquarters. NEM decided to reward its shareholders with a 79% dividend increase.The world’s number two gold miner, Barrick Gold, has already increased itsdividend three times in 2019-20. Its stock is up 56% year to date. Kinross hasnearly doubled in value, up 96% so far.

Acquisitions

How will the major goldminers spend their nest eggs, which at $2,000 gold, are becoming ever larger?There’s a very good chance they are going to spend a fair chunk on acquiringnew mines and new development properties.

Even before the goldrally picked up steam, M&A in the gold space was well underway.

Canadian precious metalsminer SSR Mining acquired Alacer Mining in all-stock, no-premium deal valued at$1.7 billion; China’s Shandong Gold bought TMAC Resources for $149 million; andSilvercorp Metals struck a deal to buy Colombia-focused Guyana Goldfields in acash and shares transaction worth about $105 million.

In February, AngloGoldAshanti announced plans to offload its remaining portfolio of South Africanassets, including Mponeng - the deepest mine in the world at 4 km underground -to Harmony Gold Mining. The sale turns Harmony into the country’s largest goldproducer.

March saw Vancouver-basedEndeavour Mining offer CAD$1 billion for Toronto-listed SEMAFO. Combined, thetwo entities created a top 15 gold producer and the largest in West Africa withsix operations.

Acquisitions amongst thegold producers - large, medium and small – has also trickled down to thejuniors. 2020 examples include:

Seabridge Gold, developing KSM, one of the largest copper-gold deposits in the world, completed the purchase of Golden Predator’s 3 Aces project in Canada’s Yukon territory.AngloGold Ashanti completed its option to purchase the Silicon project in Nevada from Renaissance Gold.Colombia-focused Caldas Gold acquired the Juby gold project, consisting of 14,000 patented claims within the Abitibi greenstone belt in Ontario. Under the deal, Caldas will issue private company South American Resources 20 million shares, and pay CAD$9.5 million to Lake Shore Gold, a subsidiary of Pan American Silver. Caldas is a spin-off of Gran Colombia Gold.“There has been anoticeable uptick in behind the scenes activity and as the COVID-19 travelrestrictions ease off, we will see an even greater number of transactions beingannounced. The increase in the gold price and company share prices has givenboth for buyers and sellers the confidence to transact,” a Canadian investmentbanker told Mining Journal.

Data from S&P GlobalIntelligence shows that so far this year, there has been a total of US$3.9billion in gold transactions, in 8 deals representing about 32 million ouncesof gold reserves. Buyers are paying an average of $123/oz.

What is prompting goldminers to acquire other miners and earlier stage assets?

The top gold producersare running out of reserves, it’s not surprising, much of the easy-to-mine goldhas been discovered.

According to McKinsey& Company, in the 1970s, ‘80s and ‘90s, the gold industry found at leastone +50Moz gold deposit and at least ten +30Moz deposits. However, since 2000,no deposits of this size have been found, and very few 15Moz deposits.

In its latest report, Wood Mackenzie says to avoid a perpetual decline inmined gold the industry will need to commission 8Moz of projects, meaning aninvestment of about $37 billion over the next five years.

However rather thanseeing another mega-merger, the likes of the Barrick-Newmont joint venture inNevada, the $10 billion fusing of Newmont and Goldcorp, or Kirkland Lake Gold’s$4.9 billion purchase of Detour Gold, at AOTH we think the more likely scenariois for senior producers to acquire development-stage juniors.

Peak gold

For years we’ve beenpredicting it. We were one of the first to say it, and now it’s coming true.But what does peak gold actually mean? AOTH did some detective work to findout.

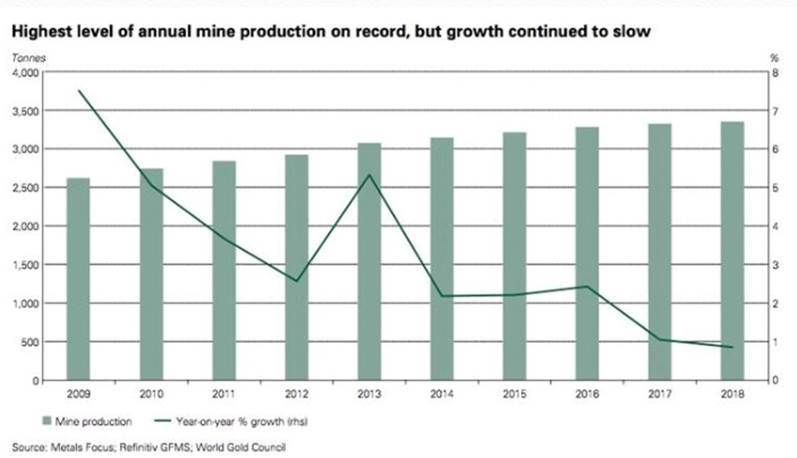

Conventional wisdomholds that peak gold is the point when the amount of gold supply hits aceiling, then stops increasing. By this definition, gold has been increasing,year by year, although by smaller and smaller amounts – supporting the idea ofthe gold supply slowly building to a top.

So, while gold outputin 2018 was higher than 2017, it was only 1% higher - 3,347 versus 3,318tonnes, according to the World Gold Council. Gold production of 3,318t in 2017was 1.3% more than 2016’s output of 3,274t. This phenomenon is showngraphically below.

But if we define peakgold as the point when mined supply no longer meets gold demand, the goldmarket peaked a long time ago. Allow me to explain.

Last year (2019) golddemand reached 4,355.7 tonnes.

WGC reports that 2019mine production was 3,463.7t.

Gold jewelryrecycling was 1,304t, bringing total gold supply last year to 4,776.1t.

If we stop there, weshow a slight gold supply surplus of 420 tonnes. Peak gold debunked!

Not so fast, let'sthink about those numbers for a minute. In calculating the true picture of golddemand versus supply, we, at Ahead of the Herd don’t, and won't, count jewelryrecycling. What we want to know, and all we really care about, is whether theannual mined supply of gold meets annual demand for gold. It doesn’t! When westrip jewelry recycling from the equation, we get an entirely different result.ie. 4,355 tonnes of demand minus 3,463 tonnes of production leaves a deficit of892 tonnes.

This is significant,because it's saying even though major gold miners are high-grading theirreserves, mining all the best gold and leaving the rest, they still didn'tmanage to satisfy global demand for the precious metal, not even close. Only byrecycling 1,304 tonnes of gold jewelry could gold demand be satisfied.

Now the questionbecomes, how do we close that predicted Wood Mackenzie 8moz mined shortfalland 900-tonne (for round numbers) jewelry supplied gap?

Through mergers andacquisitions (M&A), larger gold mining companies typically buy smaller minersto bulk up their depleting reserves base. But this doesn’t really add to theglobal supply of gold; it simply moves a portion of global reserves from onecompany to the other.

Juniors find new gold mines

A junior resource company’s place in the mining food chainis to acquire projects, make discoveries and advance them to the point when alarger mining company either buys the much de-risked project, or takes thejunior over. Understand that today’s junior resource companies own most ofthe projects that are tomorrow’s mines.

It used to be that major gold companies had large budgets withwhich to conduct exploration to replace and expand their reserves. After thegold market crash in 2012, austerity programs demanded cuts to explorationbudgets.

“The effect of thisreduced spend and limited scope meant that mining companies were barely able toreplace produced ounces while converting nearby resources to reserves,” arecent report from McKinsey & Co. states.

Moreover, the majorsshifted their attention to brownfield projects (past producers) from morerisky greenfields (undeveloped projects), leaving that to the goldjuniors.

Junior resource companies, not majors, own the worlds future minesand juniors are the ones most adept at finding these future mines. They alreadyown, and find more of, what the world’s larger mining companies need to replacereserves and grow their asset base.

Up to now the few buyouts that have occurredhave come at low premiums, or in some cases, no premiums.

But competition for ounces in theground is going to drastically heat up resulting in bidding wars and muchhigher premiums offered than we have seen to date.

Another thing that’s changed with themuch higher gold price, is major gold companies can afford to pick up smallerdeposits. Previously when gold was, say, US$800.00 majors needed to buy largedeposits, greater than several million ounces, then scale them up to have an effecton their bottom lines. With gold prices of +$2,000/oz, they could consider a500,000-oz deposit, as long as the grades are decent and it’s close to existinginfrastructure. This opens up the field to many more take-over possibilities -every company with a +500Koz gold deposit is now a potential candidate.

For Ahead of the Herd (AOTH) investors,this is a period when remarkably easy money is made if you can identifyexisting assets that are likely to be rerated in this bull market.

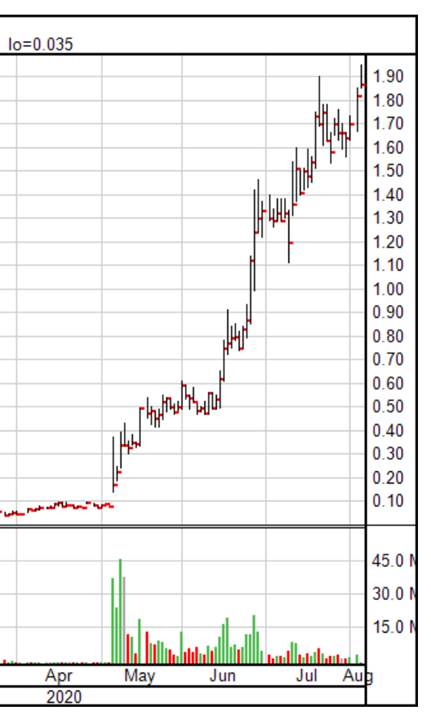

One junior we recently delivered to AOTH’s free newsletter is - Freegold Ventures (TSX-V:FVL).

The company had 6.5 million ounces ofgold in an historic resource that people had forgotten about until theyreleased a new discovery hole; the stock rocketed from $0.20 to $1.45. Itwasn’t just because they drilled a new hole, it was because the asset theyalready had was being rerated in this new market cycle. Freegold isn’t doneyet, in fact we think they are just getting started tagging on a new discoveryto an (until now) under-appreciated asset. The deposit could easily grow to 10million ounces.

There are loads more companies likethis still raising their first meaningful capital in years that will findthemselves back in the spotlight as boots hit the ground and the drills startturning. And when assay results start to roll in, the market will have to blendthe value of these new results with assets that were far underpriced in theprevious market, ie., a significant rerating will occur.

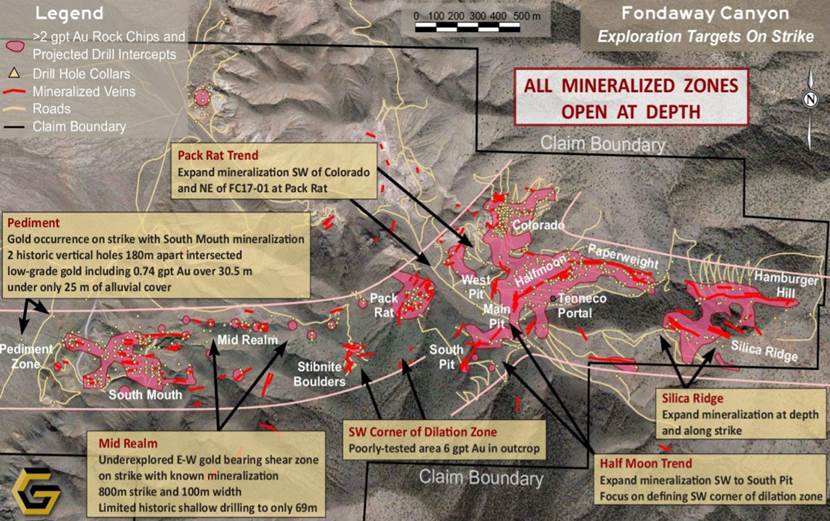

A great example is Getchell Gold (CSE:GTCH). At its Fondaway Canyon project inNevada, the high-grade resource begins near surface, is open at depth, andalong strike.

A 2017 technical report denotes 409,000oz of indicated resources grading 6.18 grams per tonne, and 660,000 oz inferredgrading 6.4 g/t, for a combined 1.1 million ounces.

That alone is impressive. But whatreally stands out, is the opportunity to add significantly more ounces if thestructures, and ultimately, the potential source of this gold system can beidentified, mapped and drilled.

The majority of the 1.1 million ouncesare hosted by the Paperweight, Halfmoon andColorado zones, with the remainder in parallel veins or splays of the majorveins - which range from 5 to 20 feet.

There is a good possibility that the veinsfound in the mountains are just the “smoke” from a major, deep-seated goldsystem. Fondaway Canyon is a strong contender for building ounces - both underground and open-pit.

To me the idea is to buy as manyIndicated and Inferred (I&I) ounces as you can, paired alongside massiveupside exploration potential. Nevada-basedGetchell Gold seems to be the perfect example. Not only does the company haveample gold resources with tremendous expansion potential, it has yet to berecognized by the market.

An unprecedented wave of acquisitionsis about to wash over the junior resource sector. The first round of major mergershas occurred, treasuries are stuffed to overflowing. Now the smaller companiesare going to be “BUY” targets and in particular the development-stage juniors.

Mergers and acquisitions activity atthe producer level usually grab headlines, not surprising considering thattake-over bids are often in the hundreds of millions, even billions of dollars.

But it is consolidation at the juniorlevel where some serious money can be made.

What are the exploration plays we thinkare going to move, based on our analysis and their drill results? Anyone canmake a 2 or 3-timer in a bull market that raises all boats. Put another way, ifthe breeze is stiff enough even turkeys can fly, but it is a rare talent whocan cast a well-trained eye over a company's drill assays, surface samples, orgeophysical surveys, to understand the rocks they're in, and thecharacteristics of the mineralization – Does it continue? Does the deposit“hang together? Is it scalable? Is it economic at today's prices? And mostimportantly, does it have “legs”, to borrow a term from journalism, to become along-term play? ie., the potential of being developed into an asset that majormining companies will be interested in acquiring?

The point at which these questions canbe answered in the affirmative, is usually when the big institutional moneycomes rushing into a stock, driving its trading volume and stock price to newheights.

Using geological expertise to identifythese projects and companies, the ones with staying power, can be highlyrewarding.

By Richard (Rick) Mills

If you're interested in learning more about the junior resource and bio-med sectors please come and visit us at www.aheadoftheherd.com Site membership is free. No credit card or personal information is asked for.

Richard is host of Aheadoftheherd.com and invests in the junior resource sector. His articles have been published on over 400 websites, including: Wall Street Journal, Market Oracle,USAToday, National Post, Stockhouse, Lewrockwell, Pinnacledigest, Uranium Miner, Beforeitsnews, SeekingAlpha, MontrealGazette, Casey Research, 24hgold, Vancouver Sun, CBSnews, SilverBearCafe, Infomine, Huffington Post, Mineweb, 321Gold, Kitco, Gold-Eagle, The Gold/Energy Reports, Calgary Herald, Resource Investor, Mining.com, Forbes, FNArena, Uraniumseek, Financial Sense, Goldseek, Dallasnews, Vantagewire, Resourceclips and the Association of Mining Analysts.

Copyright © 2020 Richard (Rick) Mills - All Rights Reserved

Legal Notice / Disclaimer: This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified; Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Richard Mills only and are subject to change without notice. Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, I, Richard Mills, assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this Report.

© 2005-2019 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.