Does Gold Really Care Whether Coronavirus Brings Us Deflation or Inflation? / Commodities / Gold & Silver 2020

One of the many bothering issues about the coronavirus crisis, is whether it will turn out to be inflationary or deflationary. What do both of these scenarios mean for gold ahead?

US Inflation Rate Declines in March

Many people are afraid that the coronavirus crisis will spur inflation. After all, the increased demand for food and hygiene products raised the prices of these goods. Moreover, the supply-side disruptions can reduce the availability of many goods, contributing to their increasing prices.

On the other hand, the current crisis results not only from a negative supply shock, but also from a negative demand shock. As a result of uncertainty, people cling to cash and forego unnecessary expenses. In addition, social distancing means reduced household spending on many goods and services, which exerts deflationary pressure. The most prominent example is crude oil, whose price has temporarily dropped to just $20 a barrel (although this was partly due to the lack of agreement between OPEC and Russia). Lower fuel prices will translate into lower CPI inflation rate. Entrepreneurs, especially those with large stocks of goods, will probably lower prices to encourage shopping. Moreover, the appreciation of the US dollar means lower prices of imported goods.

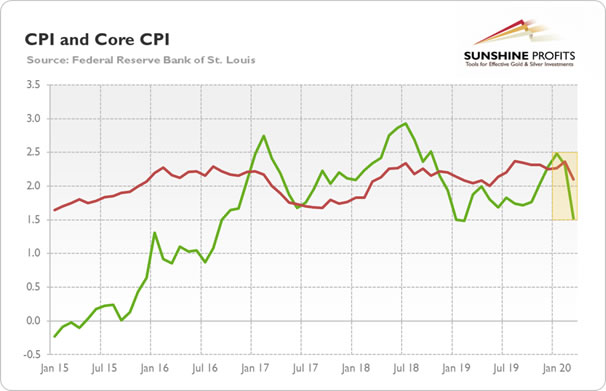

So, the disinflation pressure should prevail in the short term – and indeed, the first inflation readings in America (but also in other Western countries) show a decline in inflation. For example, the US CPI inflation rate declined 0.4 percent in March, following a 0.1 percent increase in February. It was the largest monthly decline since January 2015. The decrease was mainly driven by a sharp decline in the gasoline prices. However, the core CPI rate, which excludes energy and food prices, also decreased in March – by 0.1 percent (versus 0.2 percent rise in February), which was its first monthly decline since January 2010.

On an annual basis, the overall CPI increased 1.5 percent, which is a notably weaker increase than the 2.3 percent rise in February. The core CPI rose 2.1 percent over the last 12 months, compared to the 2.4 percent increase in the previous month. The chart below shows these disinflationary trends.

Chart 1: US CPI (green line) and core CPI inflation rate (red line) from January 2015 to March 2020.

So, Should We Expect Deflation?

No. I’m, of course, perfectly aware that the Great Recession was deflationary, as the CPI inflation rate plunged from 5.5 percent in July 2008 to -1.96 in July 2009. However, this crisis is different from the previous one. Neither during the global financial crisis nor during the Great Depression did we have a situation where such a large proportion of society does not go to work. So, the global quarantine with the associated limited international trade and broken supply chains imply that the productive capacity of the economy will suffer. And this may result in stagflation rather than deflation.

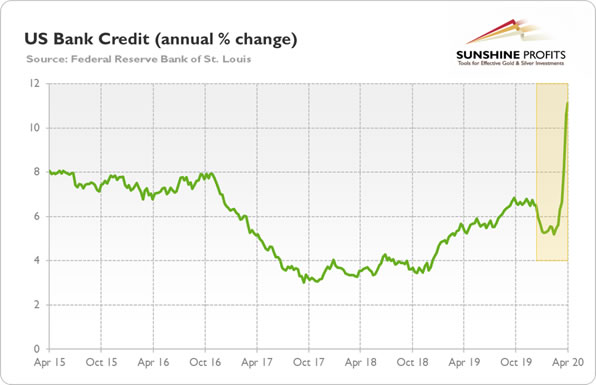

Moreover, the commercial banks are relatively healthy this time, which means that they are able to extend credit. Please note that this is the core of all emergency programs introduced by the Fed and other central banks all over the world. They encourage commercial banks to grant new loans to companies that have suffered as a result of the coronavirus crisis and social distancing. As the chart below shows, the credit supply in the US has accelerated in March.

Chart 2: US Bank credit (annual percentage change) from April 2015 to April 2020.

Given that in the contemporary monetary system new money supply is created when commercial banks extend credit, we should not exclude the risk of inflation later in the future, after the initial wave of disinflation.

Another inflationary risk factor in the longer term is the inevitable increase in federal debt, which may increase the temptation to monetize it or to strengthen the financial repression. It is widely known that the best times for governments to get out of debt is during negative real interest rates. And this can be achieved either by maintaining very negative nominal interest rates, or by increasing the inflation rate.

Therefore, while in the short term the disinflation scenario seems more likely, the risk of stagflation increases in the longer run, especially with too fast lending and excessive monetization of the debt.

Implications for Gold

What does it all mean for the gold market? Well, those who buy gold mainly as an inflation hedge do not have to worry about their holdings – inflationary monster should disappear from our economy. Remember the stagflationary 1970s? Gold soared then.

However, even if the US economy plunges into deflation, I have good news. You see, gold is not just about inflation versus deflation. The yellow metal is a safe-haven asset which may shine during both inflationary and deflationary periods. After all, gold also rallied in the aftermath of the Lehman Brothers’ bankruptcy, when the economy plunged into deflation for a while. Why? Well, gold’s price is also sensitive to market sentiment and risk aversion. Then, gold is no one’s liability. So, when deflation is accompanied by significant economic worries and a loss of confidence in the US dollar, gold may shine. Anyway, gold’s future – in a world of negative real interest rates, elevated risk aversion and high public debt – looks bright.

If you enjoyed the above analysis, we invite you tocheck out our other services. We provide detailed fundamental analyses of thegold market in our monthly Gold Market Overview reports andwe provide daily Gold & Silver Trading Alerts with clearbuy and sell signals. If you’re not ready to subscribe yet and are not on ourgold mailing list yet, we urge you to sign up. It’s free and if you don’t likeit, you can easily unsubscribe. Sign uptoday!

Arkadiusz Sieron

Sunshine Profits‘ MarketOverview Editor

Disclaimer

All essays, research and information found aboverepresent analyses and opinions of Przemyslaw Radomski, CFA and SunshineProfits' associates only. As such, it may prove wrong and be a subject tochange without notice. Opinions and analyses were based on data available toauthors of respective essays at the time of writing. Although the informationprovided above is based on careful research and sources that are believed to beaccurate, Przemyslaw Radomski, CFA and his associates do not guarantee theaccuracy or thoroughness of the data or information reported. The opinionspublished above are neither an offer nor a recommendation to purchase or sell anysecurities. Mr. Radomski is not a Registered Securities Advisor. By readingPrzemyslaw Radomski's, CFA reports you fully agree that he will not be heldresponsible or liable for any decisions you make regarding any informationprovided in these reports. Investing, trading and speculation in any financialmarkets may involve high risk of loss. Przemyslaw Radomski, CFA, SunshineProfits' employees and affiliates as well as members of their families may havea short or long position in any securities, including those mentioned in any ofthe reports or essays, and may make additional purchases and/or sales of thosesecurities without notice.

Arkadiusz Sieron Archive |

© 2005-2019 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.