March 31, 2025

Global Mining M&A Picks Up

Author - Ben McGregor

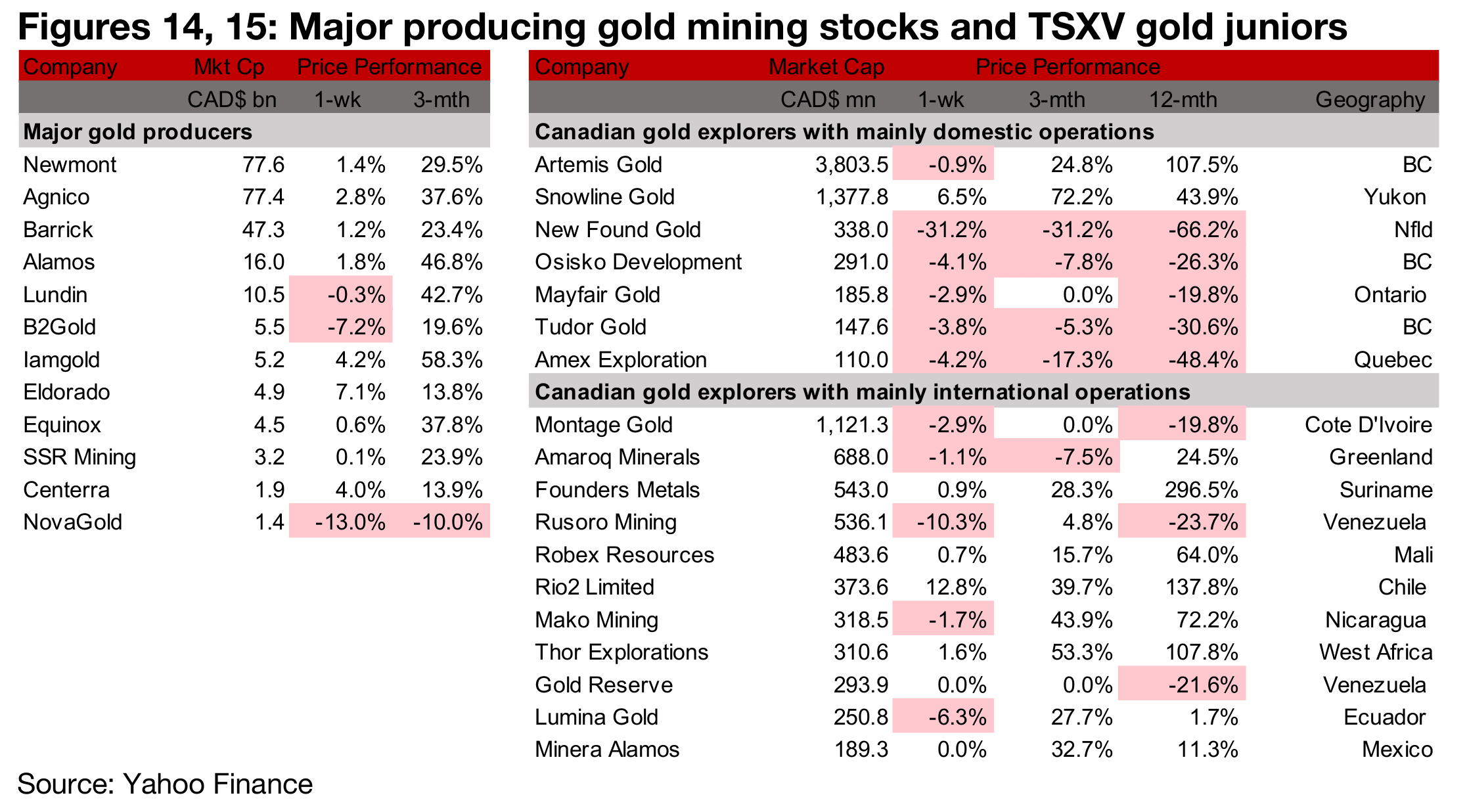

Gold stocks outperform, New Found Gold down on initial MRE

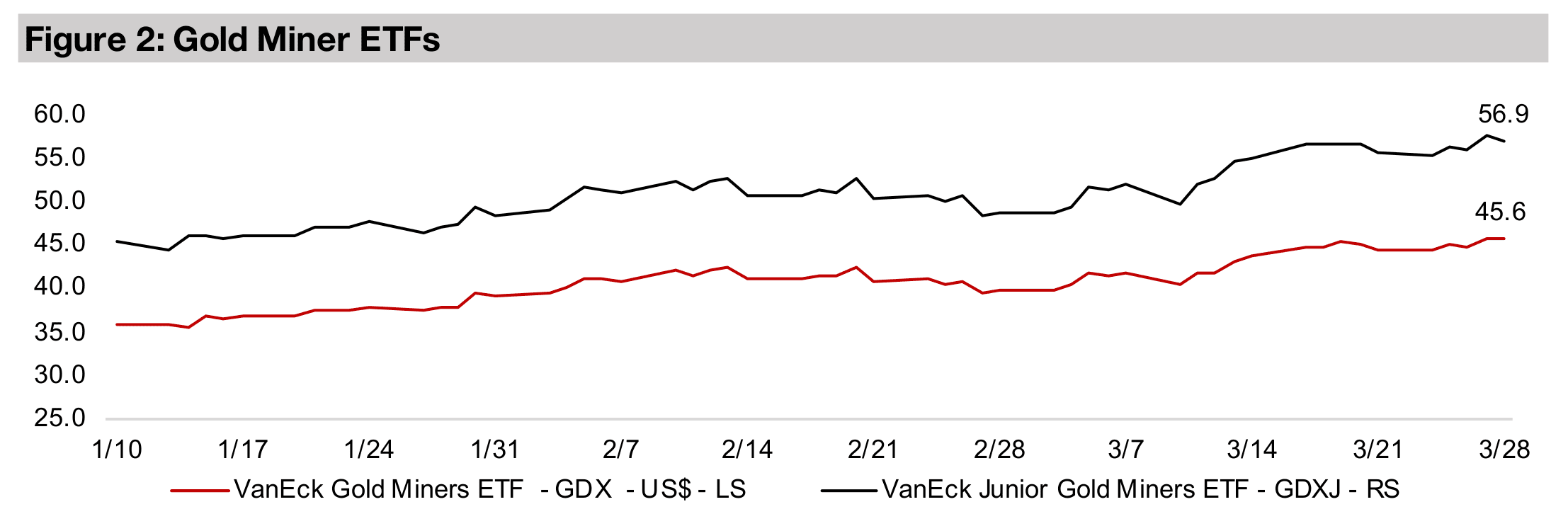

Gold stocks outperformed the equities slump, with the GDX and GDXJ up 2.4% but the S&P down -2.4%, Nasdaq off -4.0% and Russell 2000 losing -2.5%, while TSXV gold junior New Found Gold plunged -31.2% after releasing a resource estimate.

Global Mining M&A Picks Up

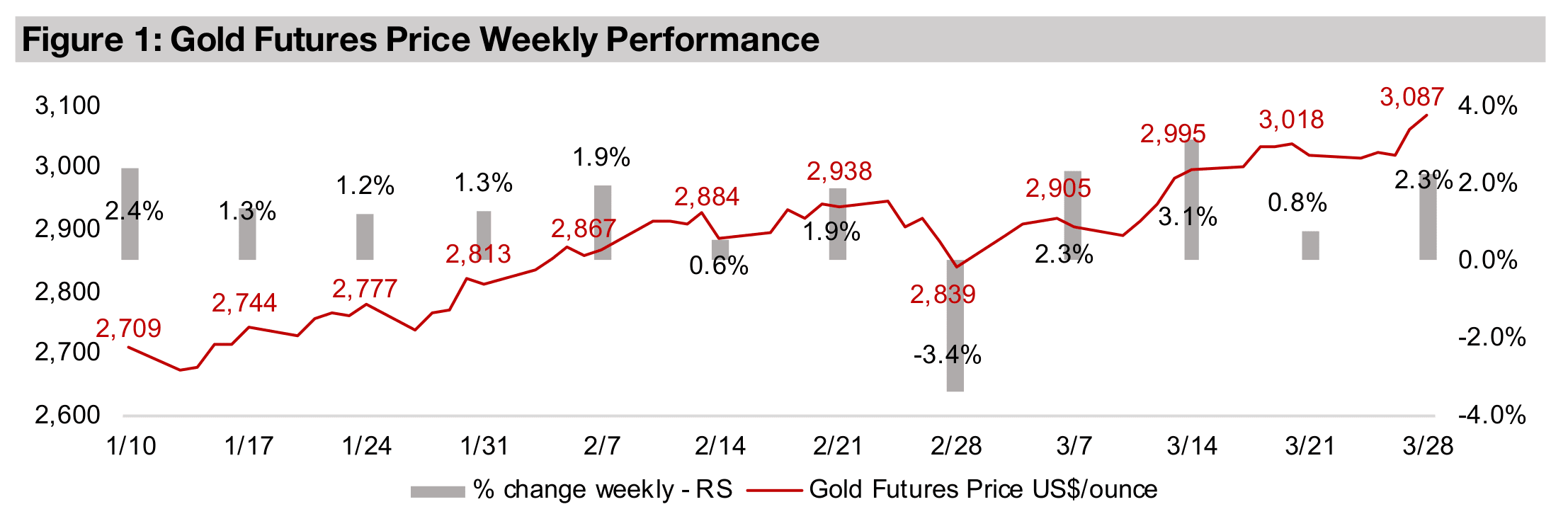

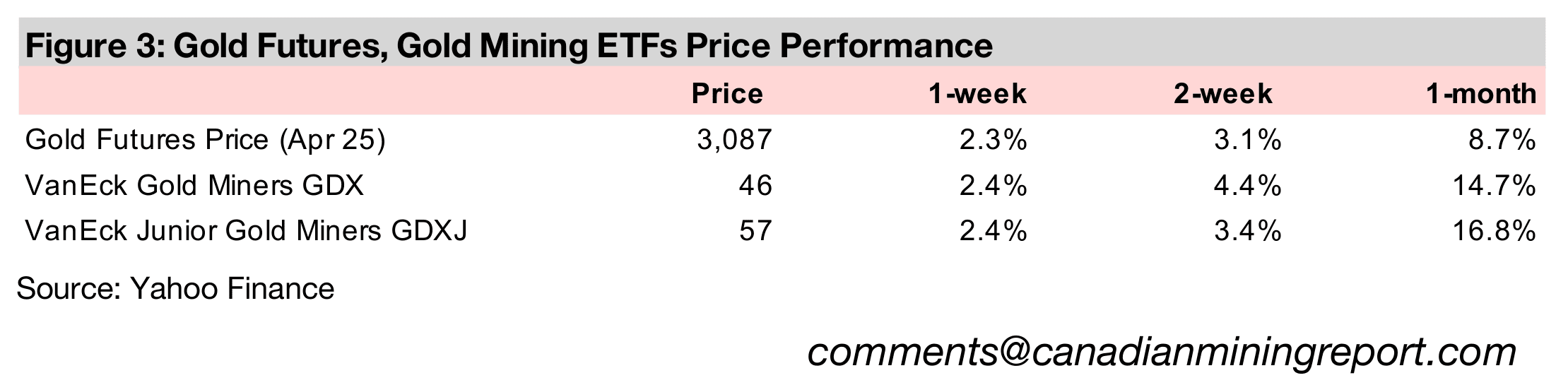

Gold rose 2.4% to US$3,087/oz, holding above the key US$3,000/oz benchmark

level for two weeks straight. The continued rise appears to be driven by a range of

factors, including tariff concerns, a slump in equity markets, and inflation which has

remained persistently above the targets of major central banks. This week saw an

upside surprise in inflation of the core personal consumption price index (PCE), which

rose 2.8% year on year, above market expectations for 2.7%. The headline PCE index

inflation rose 2.5%, inline with consensus forecasts.

Equity markets slumped on rising overall geopolitical and economic fear combined

with a tech sector that had reached exceedingly high valuation multiples. This has

continued to drive a plunge in the Nasdaq, which was down another -4.0% this week,

underperforming the -2.4% fall in the S&P 500 and -2.5% drop in the Russell 2000

index. Gold stocks continued to remain resilient in the face of the broader equity

decline, with the GDX and GDXJ both up 2.4%, indicating that the market seems to

be finally pricing in a longer period of higher gold prices. However, many of the large

TSXV gold stocks were down, suggesting that rising risk aversion and the overall

pressure on small caps is still offsetting the gain in the metal for some stocks in the

sector. Markets could be concerned especially that pre-production junior miners will

face an increasingly difficult financing environment if equity markets continue to slide.

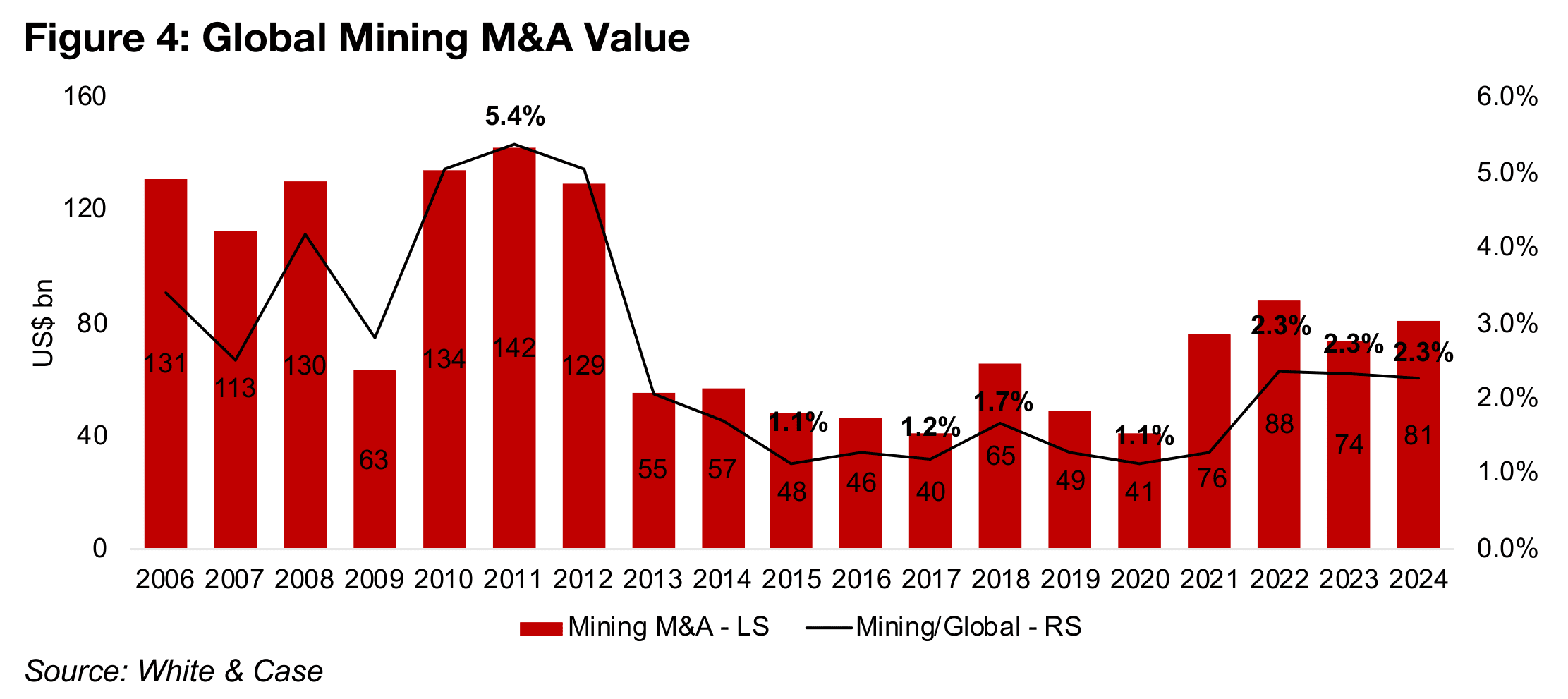

Moderate pickup in global mining M&A in 2024

Global mining M&A rose to US$81bn in 2024, up 9.5% from US$74bn in 2023, but still off the most recent peak of US$88bn in 2022, and well down from the US$142 in 2011 at the highs of the previous cycle (Figure 4). The sector’s M&A has tracked the overall level of global of M&A, with it maintaining the same 2.3% share from 2022- 2024, around twice the level of the lows just above 1.0% in the mid-2010s, but down from the 5.4% highs in 2011.

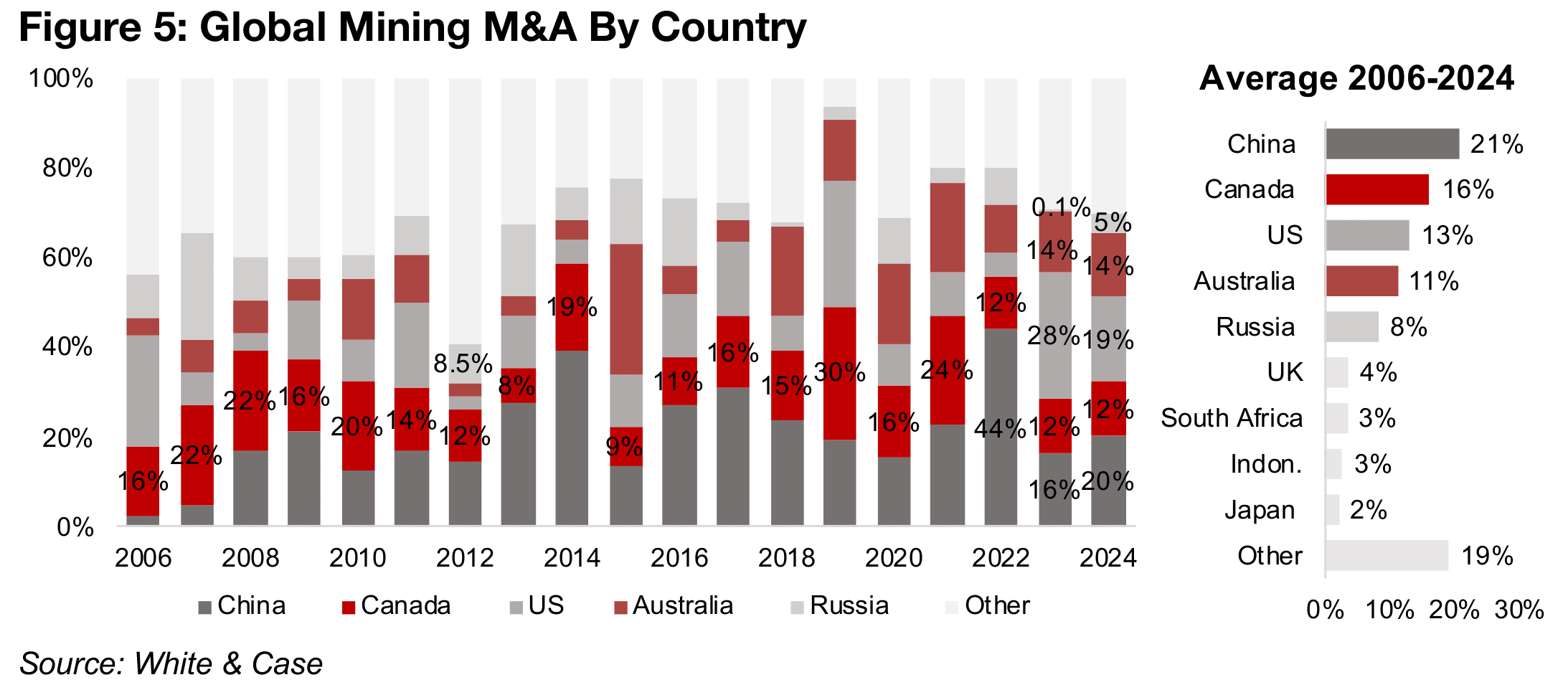

There have been five major M&A mining players over the past two decades, China,

averaging 21% of the deal value from 2026-2024, Canada, at 16%, the US, at 13%,

Australia, at 11% and Russia, at 8% (Figure 5). However, Canada and Australia are

by far the leaders based on M&A to GDP, given their high deal value but small

economic size. The share of mining M&A in 2024 for most of the major players

remained relatively stable, with China rising to 20% from 16%, Canada and Australia

flat at 12% and 14% and only the US seeing a significant decline to 28% from 19%.

It is unclear how a shift towards global protectionism may affect mining M&A from

2025. Both the US and China seem to be turning more towards a focus on their huge

markets, which could see a rise in domestic M&A. While both Canada and Australia

do have large domestic mining industries, global investment is still extremely key for

the sectors in both countries and could see them remain internationally focused.

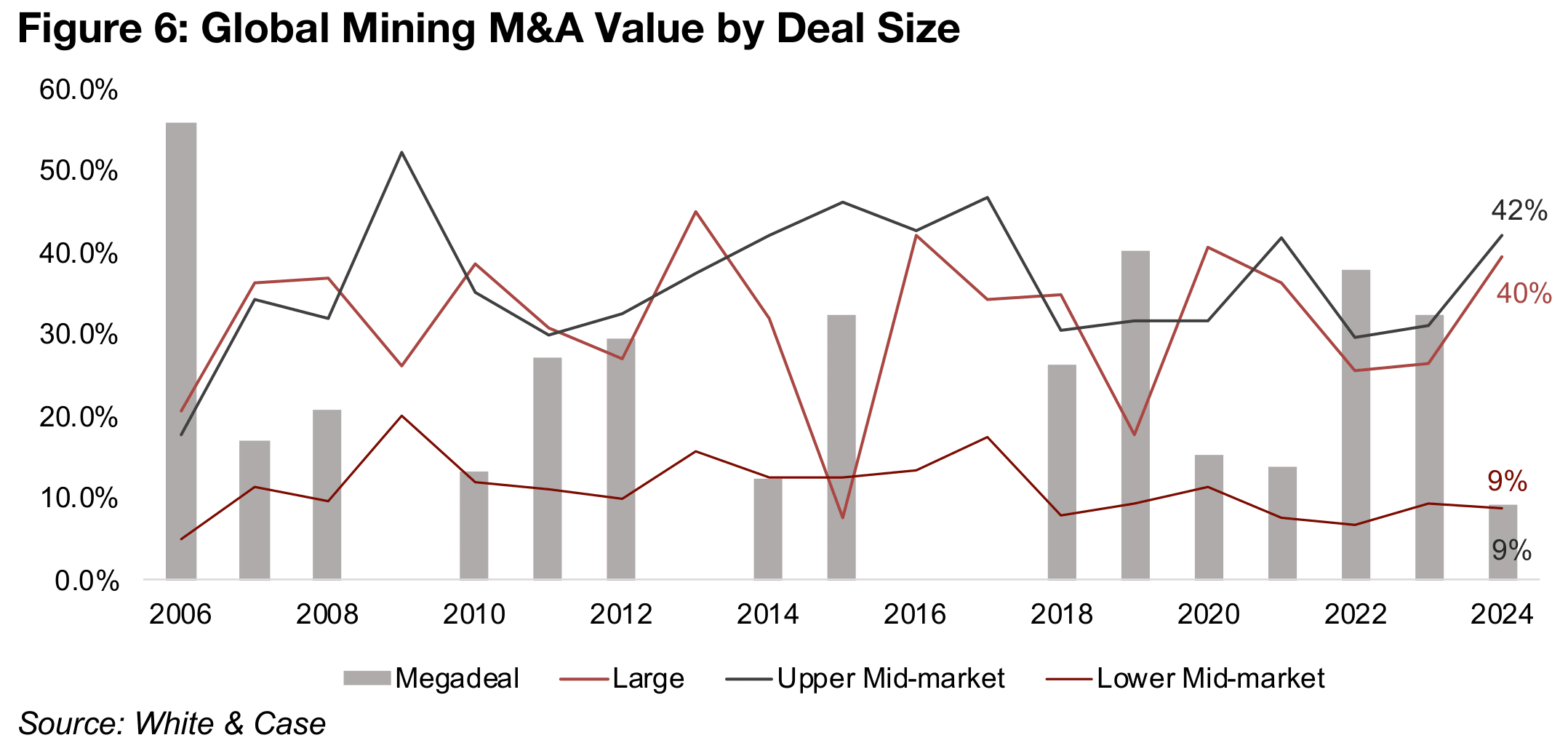

There was a clear shift away from megadeals in 2024, which were just 9% of the total M&A value versus 33% in 2023 and 38% in 2022, given a limited number of such huge potential deals (Figure 6). The market shifted to towards large deals, at 40% of the total in 2024, after 27% in 2023 and 26% in 2022, and upper mid-market deals, at 42% of the total, up from 31% and 39% over the same periods. Lower mid-market deals have had a relatively consistent share since 2018, ranging from 7.6% to 11.5%.

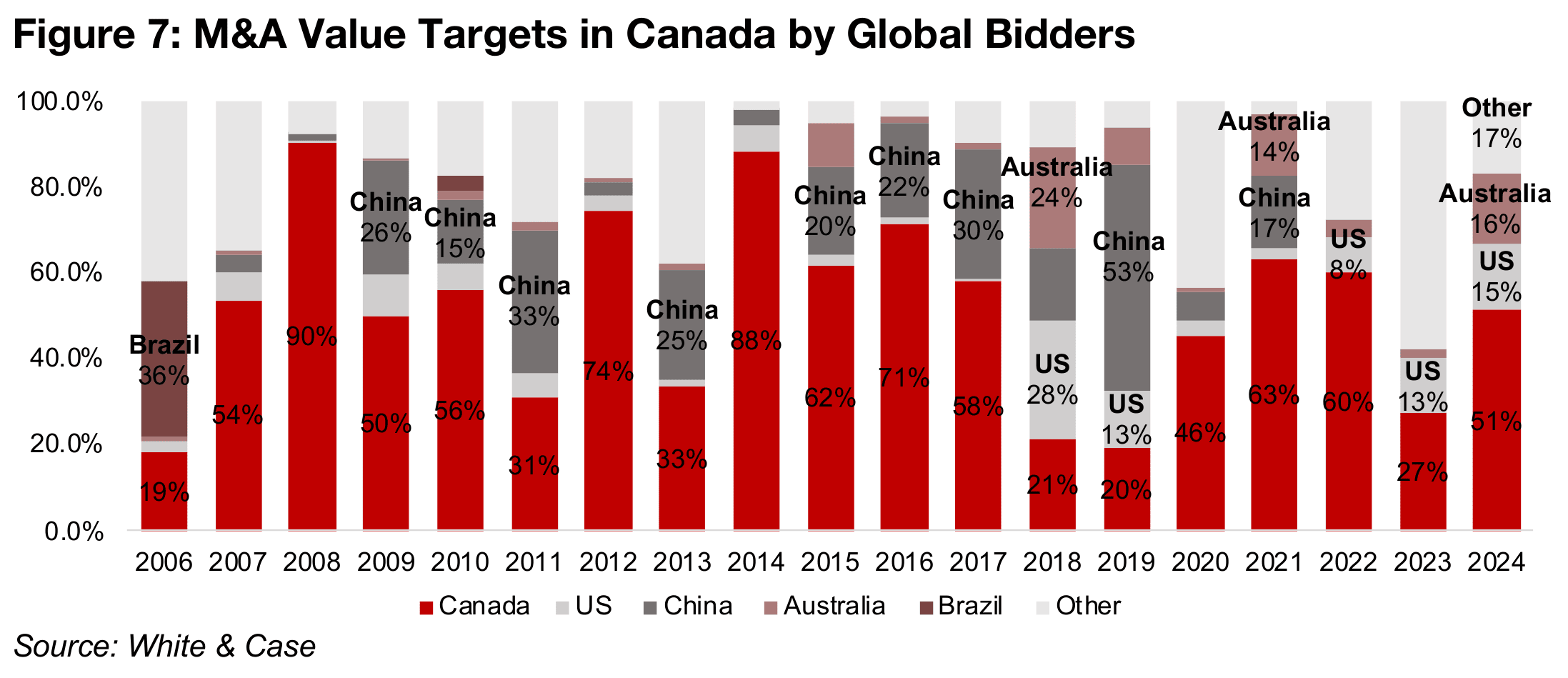

Mining M&A for Canadian targets is half from domestic investment

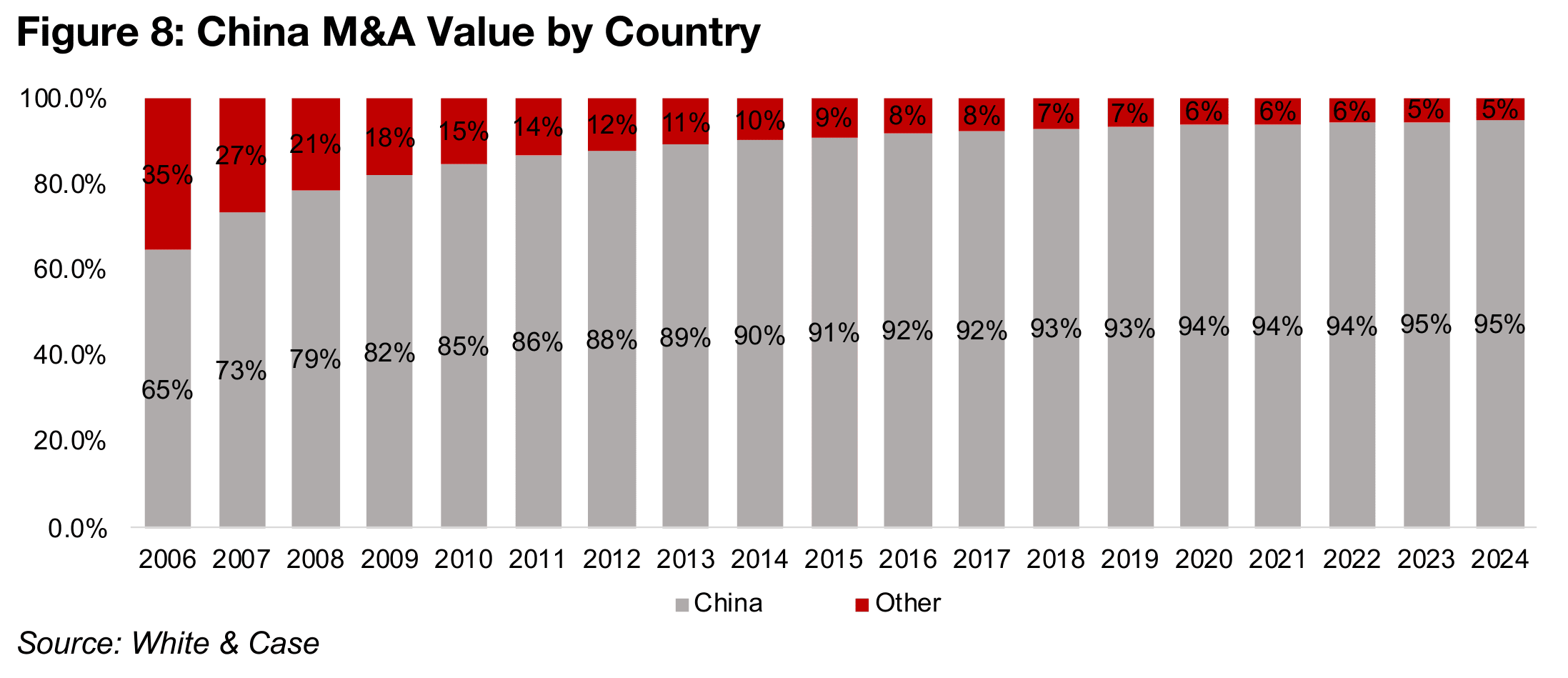

About half of mining M&A for targets in Canada has been driven by domestic investment, at 51.3% of the total from 2006-2024. This was the exact level of domestic mining M&A for Canadian targets in 2024, with Australia at 16% and the US at 15% (Figure 7). While China was a large proportion through the 2010s, its share has declined to near zero in the 2020s, part of a trend towards domestic M&A for the country, which was 95% of the total in 2024, up from 65% in 2006 (Figure 8).

Gold dominates large global mining M&A deals

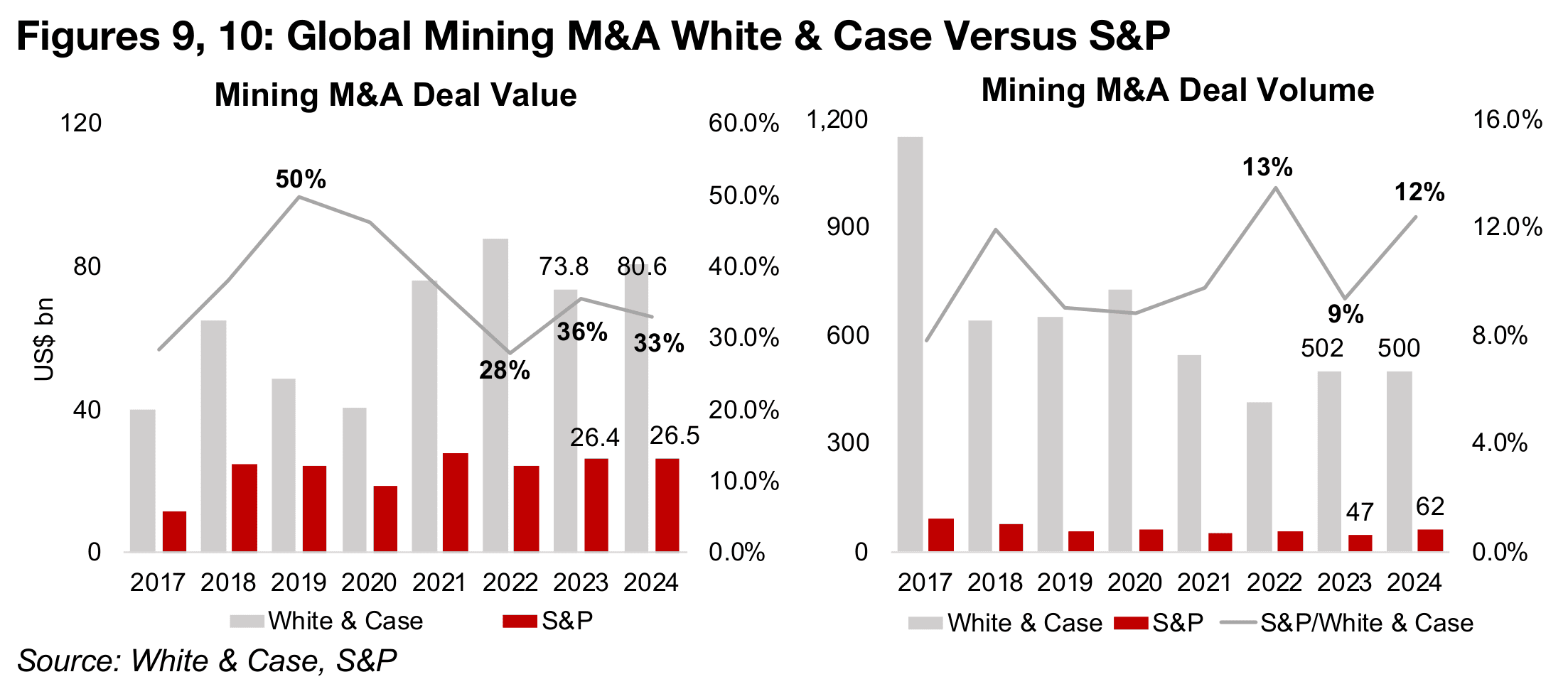

S&P also reports data on global mining M&A, but it only includes reasonably large deals, so the total reported value is just US$26.5bn, or 33% of the US$80.6bn total reported by White & Case (Figure 9). The number of deals is even smaller, at just 62, or 12% of the 500 reported by White & Case (Figure 10). The S&P data gives a more detailed look at the M&A activity, providing a split between gold and other metals.

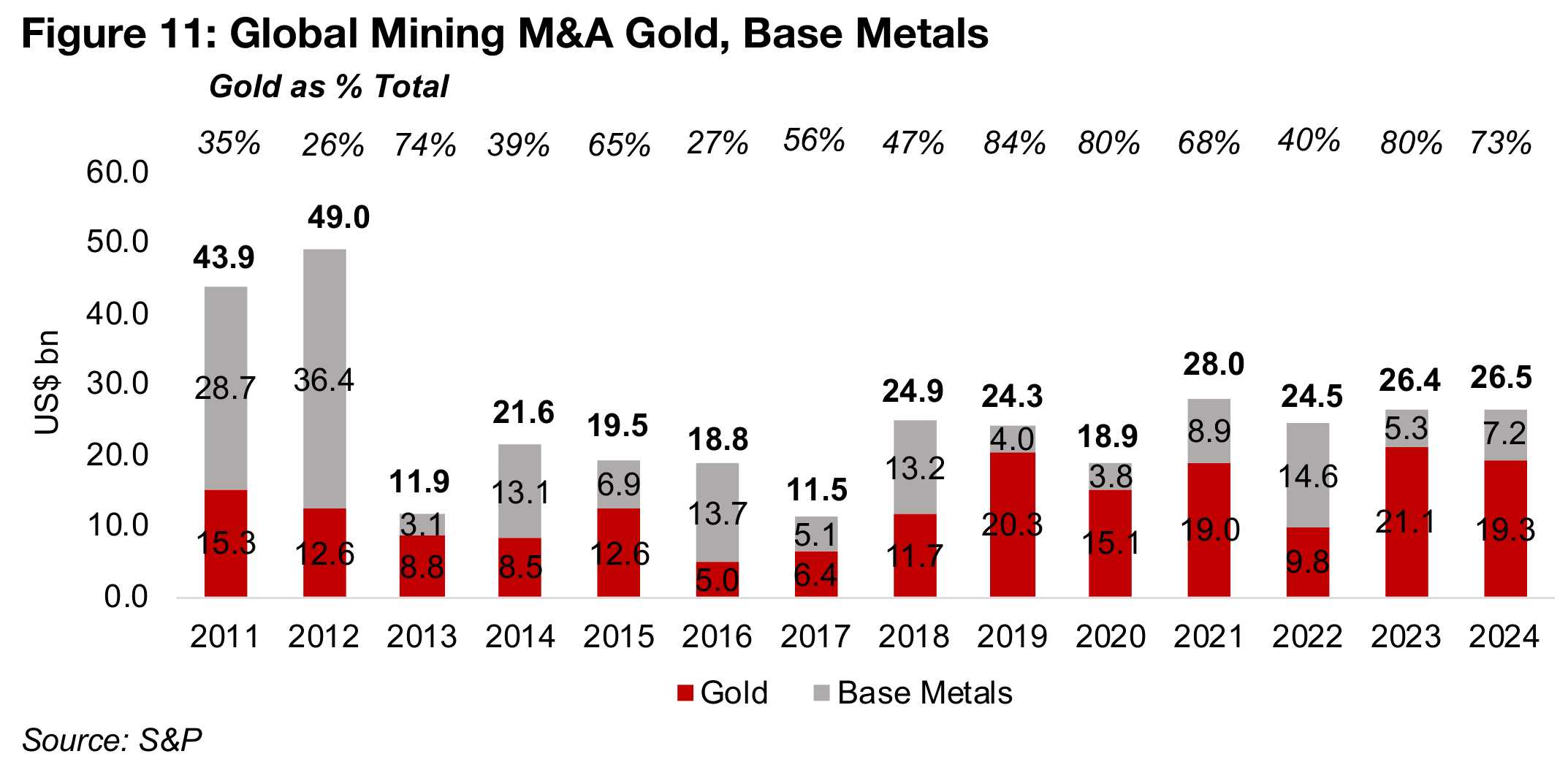

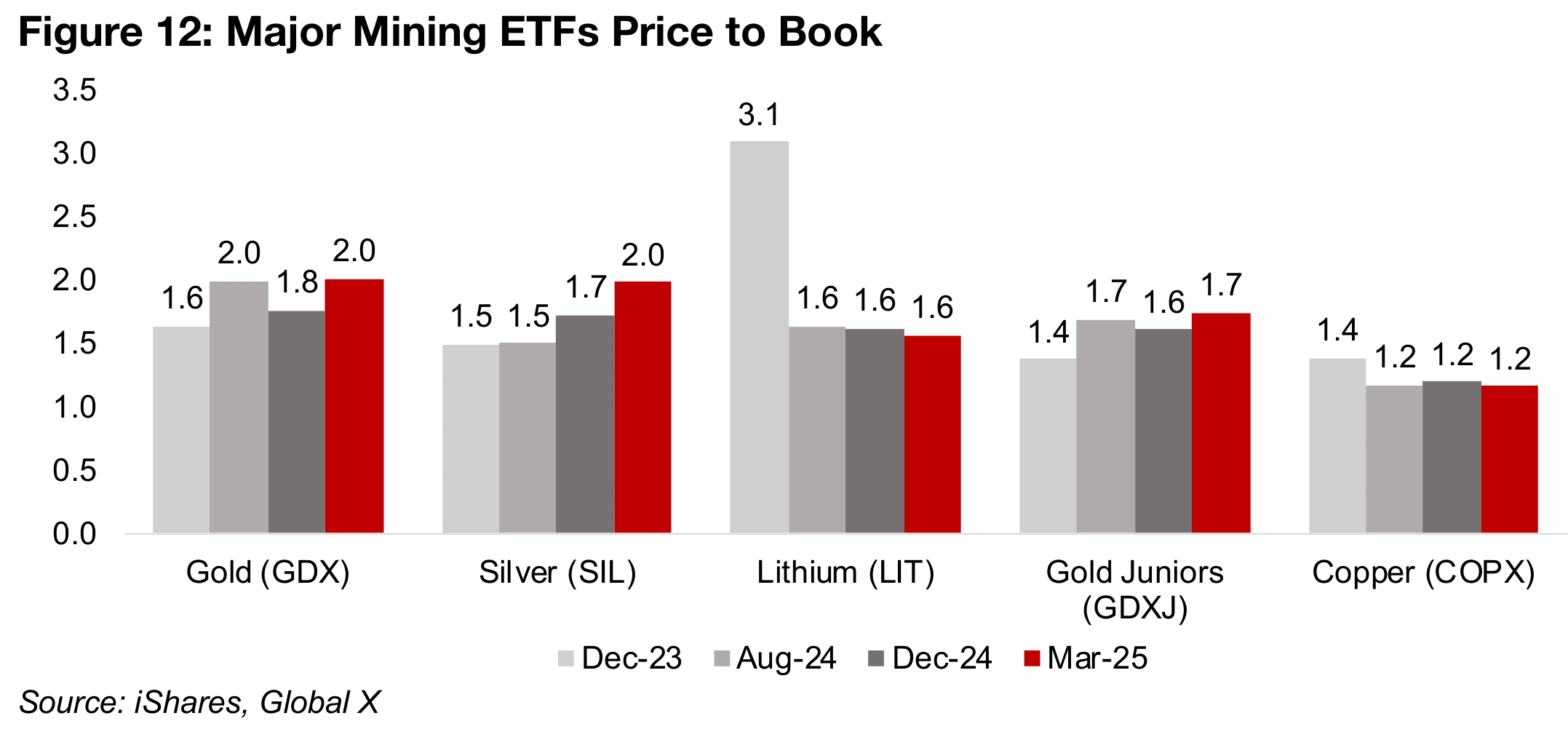

Gold was by far the leading target for large mining M&A in 2024, at US$19.3bn, or 73% of the total, although this declined from US$21.1bn in 2023, with base and other metals at US$7.2bn, or 27% of the total, increasing from US$5.3bn in 2023 (Figure 11). For 2025, there still appears to be room for further growth in M&A, given that sector valuations remain low. Even after the huge jump in the gold price, the GDX and GDXJ are trading at moderate price to book (P/B) ratios of just 2.0x and 1.7x, and the P/B for the copper ETF at just 1.2x looks particularly low (Figure 12).

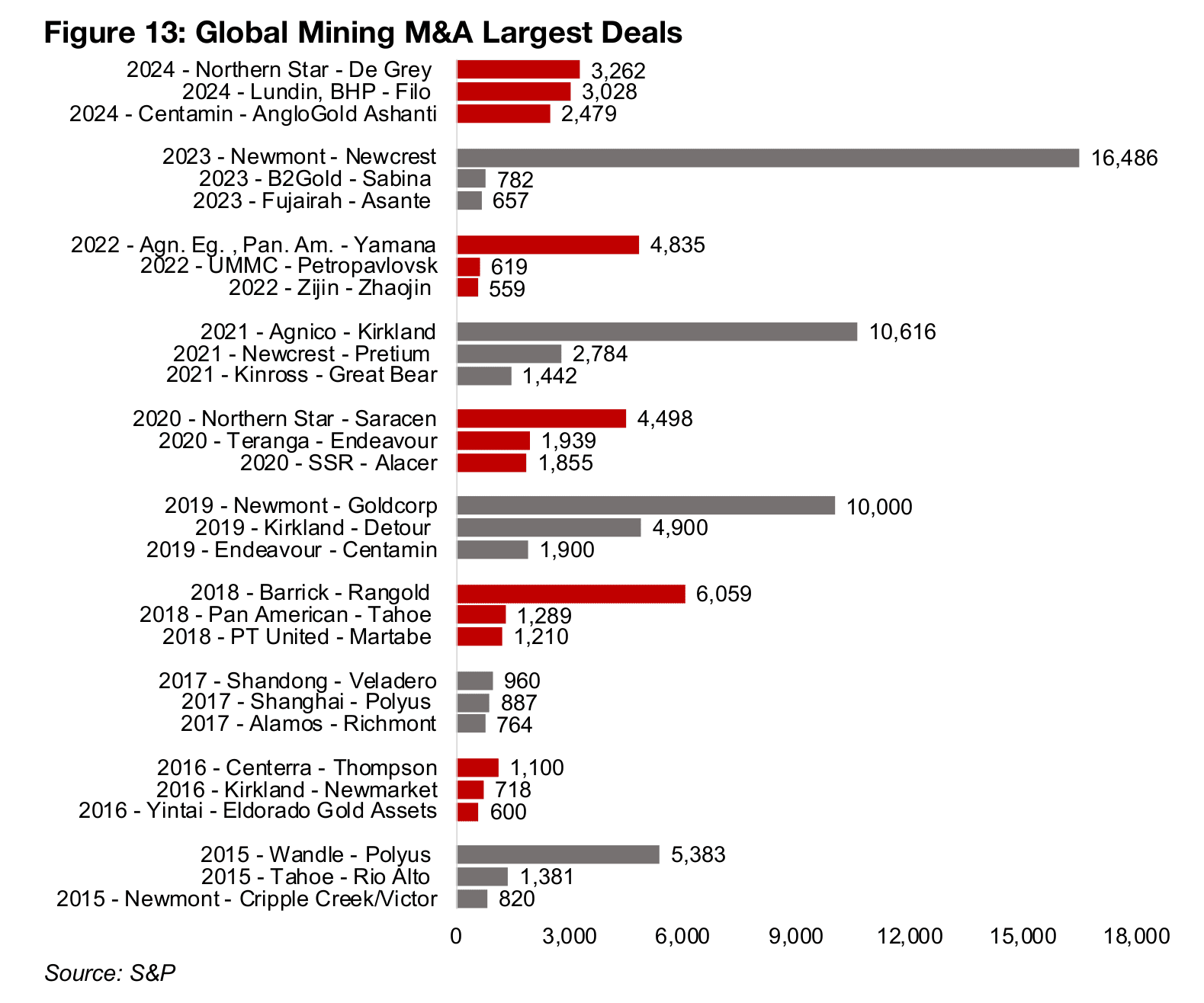

One shift in 2024 was that there were no massive deals like the acquisition of Newcrest by Newmont for US$16.5bn in 2023, Kirkland by Agnico Eagle for US$10.6bn in 2021 or Goldcorp by Newmont by US$10.0bn in 2019 (Figure 13). These huge M&A transactions do not occur every year as there are a very limited number of companies at this size which would also be an appropriate match. However, there were still three reasonably large deals in 2024, with Northern Star acquiring De Grey for US$3.3bn, Lundin and BHP buying Filo for US$3.0bn and Centamin purchasing AngloGold Ashanti for US$2.5bn.

Most major producers see gains but TSXV gold mainly down

Most of the major gold producers rose but large TSXV gold mainly declined (Figures

14, 15). For the TSXV gold companies operating domestically, New Found Gold was

down -31% on the release of its long awaited Queensway initial mineral resource

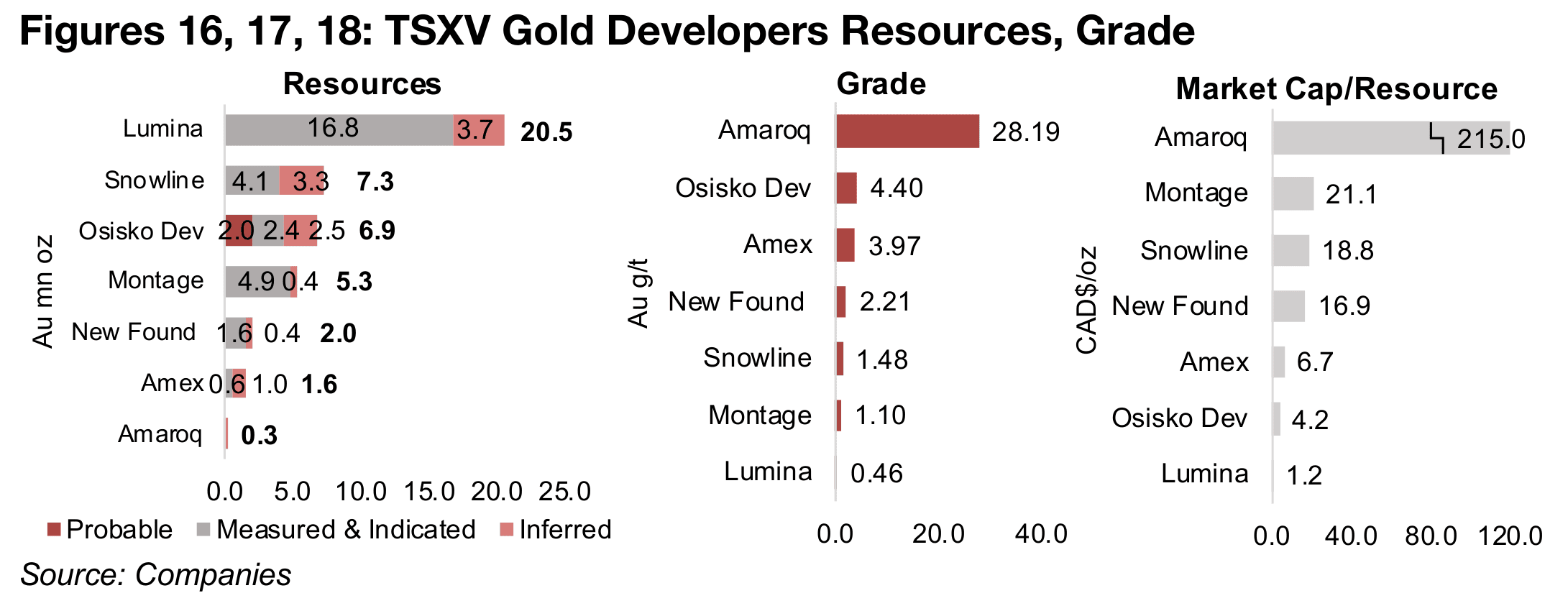

estimate. The 2.0 mn oz Au resource puts it around the middle of the TSXV gold

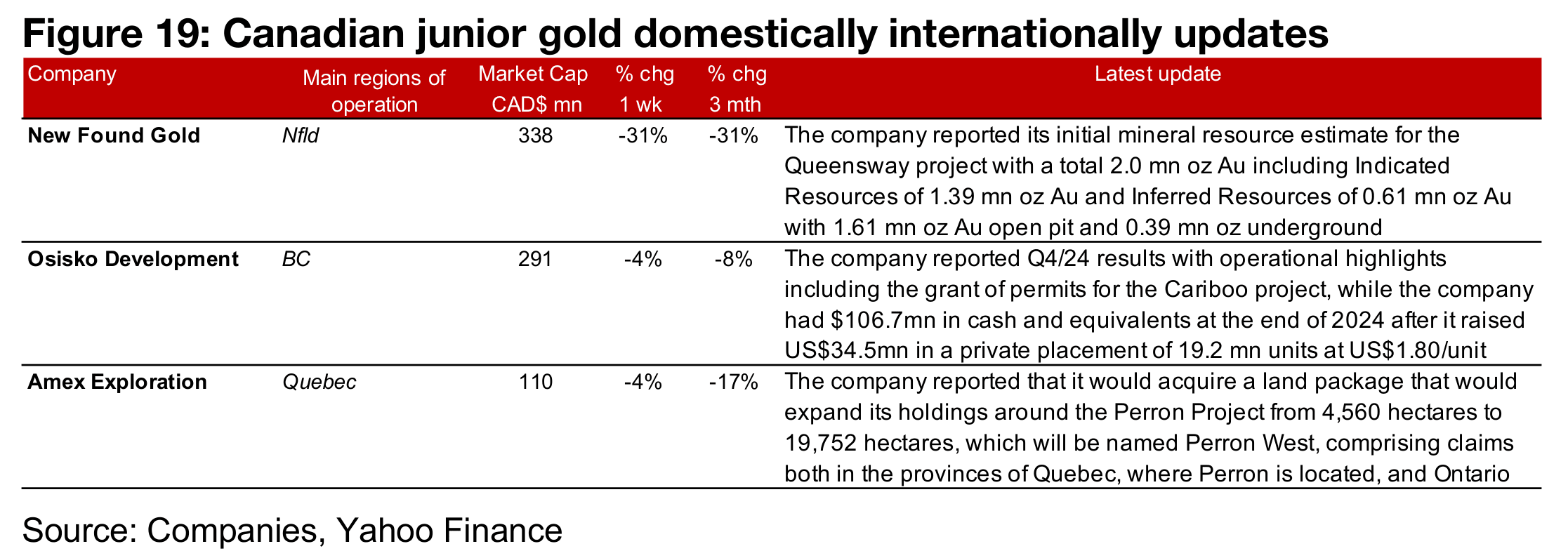

developers for size, grade and market cap to resource (Figures 16, 17, 18). Osisko

Development reported Q4/24 results and Amex Exploration announced a large

expansion of Perron’s land package (Figure 19).

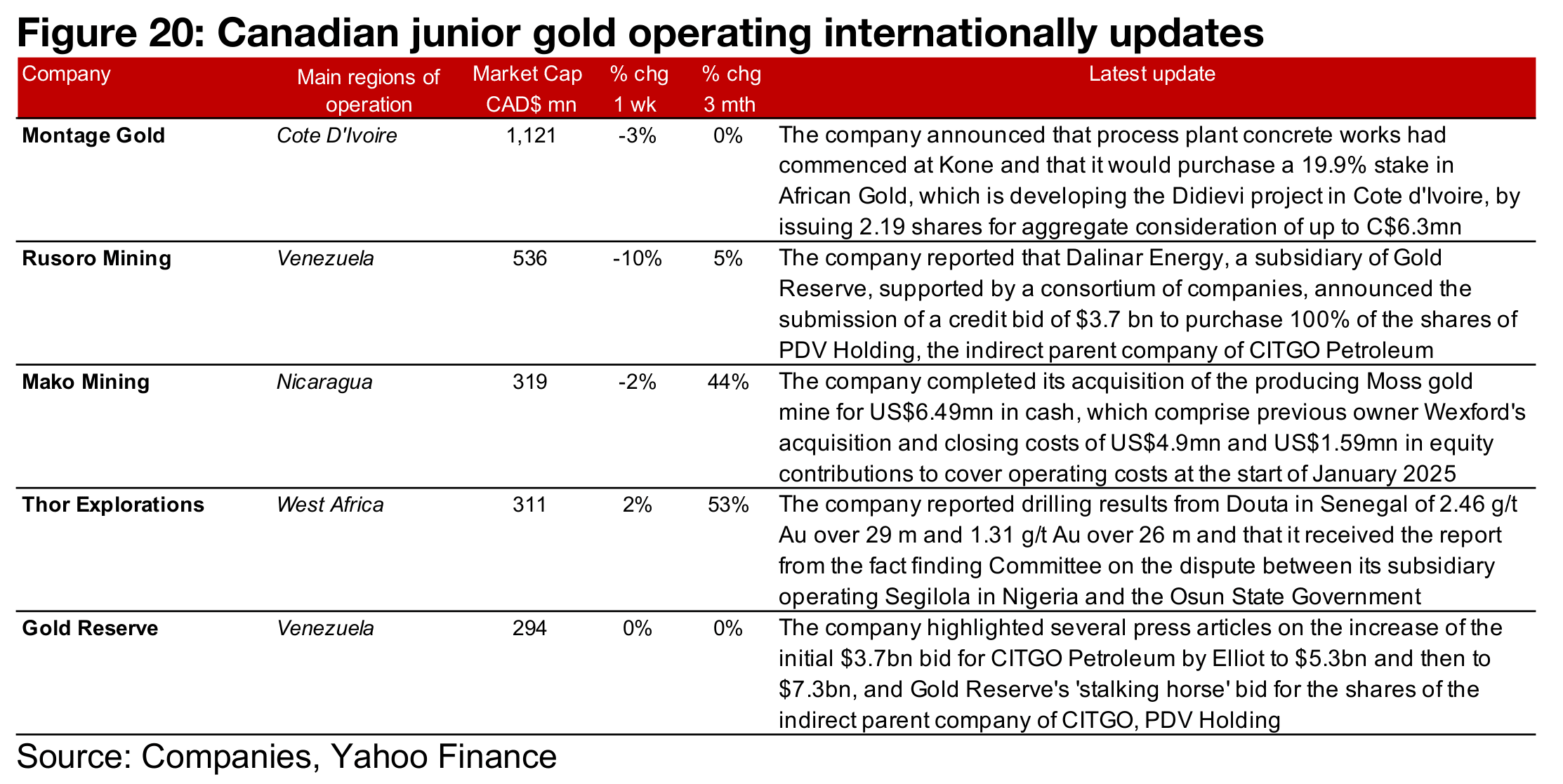

For the TSXV gold companies operating internationally, Montage Gold reported that

process plant concrete works had started at Kone and that it would purchase a stake

in African Gold, which operates the Didievi project. Rusoro and Gold Reserve both

made announcements on the auction of CITGO and Mako Mining closed its

acquisition of the Moss Mine. Thor reported drilling results from Douta and that it

received the report from the fact-finding Committee between on the dispute between

its subsidiary operating Segilola in Nigeria and the Osun state government (Figure 20).

Disclaimer: This report is for informational use only and should not be used an alternative to the financial and legal advice of a qualified professional in business planning and investment. We do not represent that forecasts in this report will lead to a specific outcome or result, and are not liable in the event of any business action taken in whole or in part as a result of the contents of this report.