Toachi Mining Announces Positive PEA for Its La Mina VMS Project

Toachi Mining Inc., (“Toachi” or the “Company”) (TSX-V:TIM) (OTCQB:TIMGF) is pleased to announce the positive results of the independent Preliminary Economic Assessment (“PEA”) for the La Mina VMS Project (“Project”) located in the Province of Cotopaxi, Ecuador. The PEA was prepared pursuant to National Instrument 43-101 (“NI 43-101”) and has an effective date of March 30th, 2019. A NI 43-101 technical report summarizing the PEA (the “Technical Report”) will be available on SEDAR no later than June 20th, 2019. All references to currencies herein are in U.S. dollars.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20190430005522/en/

Figure 1 (Graphic: Business Wire)

PEA Highlights 1

- The underground mine produces diluted polymetallic mine material for processing at an 800 tonne per day capacity on-site flotation mill. The mill products (i.e. a Cu/Pb concentrate and a Zn concentrate) are sold to smelters in Asia.

- The mine plan encompasses 2 million tonnes of potentially mineable mineralization, average head grade 10 Au Eq g/t.

- The Project would operate for 7.1 years with a Net Present Value (“NPV”) (5%) of $52 million after tax, an Internal Rate of Return (“IRR”) of 24% after tax, and an after tax payback period of 3.5 years.

- The life of mine (LOM) Net Smelter Return (NSR) is $402M which equates to 318,000 troy oz Eq. based on 2 Mt milled and the projected $1,264/ troy oz Au gold price. The NSR does not include any revenue from lead contained in the Cu/Pb and Zn concentrates.

- The LOM net direct cash costs (C1) amount to $74/t milled. The Project’s C1 cash cost, on an equivalent troy oz Au/t milled basis, is $470/troy oz Eq Au.

- The All-In Sustaining Cost (AISC) is $101/t milled. The Project’s AISC, on an equivalent troy oz Au/t milled basis, is $640/troy oz Eq Au.

- The results of metallurgical testing completed to date indicate that there are opportunities for improvement in the project economics.

- The Company reports local community support for the Project with few dissenters and is engaging local communities. Ecuador has a regulatory regime for the social and environmental assessment and permitting of mines.

PEA Results Summary

| IRR Before-Tax / After-Tax | 38% / 24% | |||

| NPV @ 5% - Before-Tax / After Tax | $100 M / $52 M | |||

| NPV @ 8% - Before-Tax / After Tax | $81 M / $39 M | |||

| NPV @ 10% - Before-Tax / After Tax | $70 M / $32 M | |||

| Payback – after starting mineral processing - After tax | 3.5 years | |||

| Nominal Production rate – dry metric tonnes/day (dmt/d) | 800 tpd | |||

| Total tonnes processed LOM (dmt) | 2 million tonnes | |||

| Average head grade over life of mine (LOM) | 10 g Au Eq /tonne | |||

| Estimated Mine Life | 7.1 years | |||

| Total Gold production (payable oz) | 112,000 oz | |||

| Total Silver production (payable oz) | 1,228,000 oz | |||

| Total Copper production (payable lbs) | 92 M lbs | |||

| Total Zinc production (payable lbs) | 76 M lbs | |||

| LOM net direct cash cost (C1) ($/tonne) | $74 / tonne | |||

| All-In Sustaining Cost (AISC) ($/tonne) | $101 / tonne | |||

| Initial Capital Cost | $70.3 M | |||

| Sustaining and Closure costs | $47.6 M | |||

Cautionary note: The PEA was prepared in accordance with National Instrument 43-101 Standards of Disclosure for Mineral Projects ("NI 43-101"). Readers are cautioned that the PEA is preliminary in nature and includes the use of Inferred Mineral Resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as Mineral Reserves, and there is no certainty that the results of the PEA will be realized.

The PEA was led by independent resources, mining, metallurgy, processing and environmental consultants, with support from the Toachi technical team. The principal consultants include: SGS Canada Inc., Geological Services (“SGS”); SGS Lakefield, SGS Bateman, Brian Wolfe and Dr. Simon Strickland Meik. A number of other independent consulting firms and potential vendors also provided information used in the PEA.

Alain Bureau, President & CEO, stated, “Today’s PEA demonstrates the La Mina VMS Project is a high-return, capital efficient and low-operating cost project. This evaluation is a significant milestone, showing a polymetallic project with an After-Tax IRR of 24% and NPV (5%) of US $52 million. The PEA is based on the production of two marketable base metal concentrates with high values in precious metals. This also brings a strong foundation for Toachi to build on as the deposit is open at depth, and recent exploration indicates the possible continuity of the mineralised footprint to the north. It is important to mention the present PEA does not include the recently discovered “Guatuza zone” as well as Toachi’s plans to initiate further metallurgical and processing tests to pursue the optimization of the Project.”

PEA Results

The cash flow model is based on developing the Upper North zone of deposit, followed by the Lower North zone before mining the South zone of the deposit. The cash flow model encompasses the CAPEX and OPEX costs for mining, processing, tailing, infrastructure, G&A, and environment. The Project has a fifteen-month pre-production development period. Production ceases in year 8. The economic criteria used in the cash flow model are shown below.

| Concentrate | Production LOM - dmt | Metal | Recovery | Payable | ||||||||||||

|

Copper

20.9% Cu content |

218 dry kt | Au | 43.1% | 96% | ||||||||||||

| Ag | 47.9% | 90% | ||||||||||||||

| Cu | 89.4% | 96.5% | ||||||||||||||

| Pb | 71.6% | 0% | ||||||||||||||

| Zn | 20.0% | 0% | ||||||||||||||

|

Zinc

51.2% Zn content |

94 dry kt | Au | 26.6% | 65% | ||||||||||||

| Ag | 26.1% | 70% | ||||||||||||||

| Cu | 4.5% | 0% | ||||||||||||||

| Pb | 13.4% | 0% | ||||||||||||||

| Zn | 70.5% | 85% | ||||||||||||||

Project income is derived from the sale of the copper/lead and zinc concentrates and includes the following:

- Metal grades in each concentrate

- Logistic and transport costs

- Treatment charges

- Refining charges

- Projected 8% moisture in concentrates

- Penalties

- Minimum deductions

- Payable rates

The after tax cashflow includes deductions for the following:

- Amortization

- Ecuadorian royalty

- Income taxes

- Export duties

- Employees profit sharing

The cash flow includes the following operating costs and G&A:

| OPERATING COST | LOM average ($/t milled) | |||

| MINE | ||||

|

- Stoping cost |

$26.14 | |||

|

- Mine support operations cost |

$20.01 | |||

|

- Mine equipment lease cost |

in sustaining capex | |||

|

- Sub-total mine OPEX |

$46.15 | |||

| PROCESSING | ||||

|

- Power |

$4.22 | |||

|

- Labour |

$4.70 | |||

|

- Reagents |

$11.58 | |||

|

- Grinding media |

$3.55 | |||

|

- Repair materials and operating supplies |

$1.60 | |||

|

- Liners and wear materials |

$0.97 | |||

|

- Sub-Total Mill OPEX |

$26.62 | |||

| Tailings storage facility & effluent treatment | $1.23 | |||

| TOTAL OPEX | $74.00 | |||

| G&A | $5.15 | |||

| TOTAL | $79.15 | |||

PEA Pre-Production CAPEX

The mine CAPEX includes development, infrastructure, equipment and G&A and indirect costs. The process CAPEX includes the mill, general site infrastructure, tailings storage facility, effluent treatment plant, General & Administration (G&A) and Owners’ costs. The preproduction capital is shown below.

| AREA | ITEM | CAPEX | ||||||

| Mine | Infrastructure | $3.5 M | ||||||

| Development | $5.3 M | |||||||

| Equipment | $4.2 M | |||||||

| G&A and indirects | $4.0 M | |||||||

| Sub-Total Mine | $17.0 M | |||||||

| Mill and General Site | Process | $40.2 M | ||||||

| Tailings and effluent | Tailings & effluent treatment | $ 3.1 M | ||||||

| Sub-Total Mill & General Site | $43.3 M | |||||||

| Contingency | $10.0 M | |||||||

| Total Preproduction CAPEX | $70.3 M | |||||||

PEA Economic Analysis

IRR and NPV values were extracted from the cashflow model. Three year trailing monthly average metal prices as of January 31st, 2019 were used in the Updated Mineral Resources Estimate and the PEA cashflow model. The results of the PEA economic analysis are shown below.

| Before-tax | After-tax | ||||||||||

| IRR | 38% | 24% | |||||||||

| NPV(5%) | $100 M | $52 M | |||||||||

| NPV(8%) | $81 M | $39 M | |||||||||

| NPV(10%) | $70 M | $32 M | |||||||||

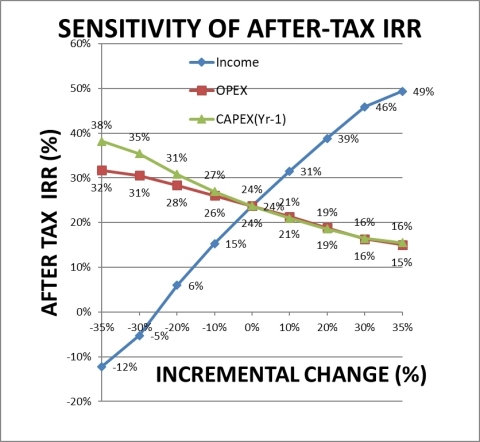

PEA Results Sensitivity

The Project is most sensitive to changes in income and less sensitive to changes in opex and capex as shown in Figure 1.

Ownership

The property is owned by Compania Minera La Plata S.A. (restructured from Sultana Del Condor Minera S.A.) and entered into an agreement with Ferrum (which later became Toachi Mining Inc.) on October 28th, 2015. Ferrum announced the signing of a letter of intent with Sultana on February 11, 2016, pursuant to which Ferrum has been granted the option to acquire up to a 75% interest in the Project over a period of four years. To earn a minimum of 60% interest, Ferrum must make cash payments totalling US$2.0 million and incur expenditures totalling US$4.0 million.

Sensitivity Analysis of the Updated Mineral Resources Estimate - Base case at 4.0 g/t Au cut-off grade

|

Cutoff (AuEq – g/t) |

Tonnage (kt) |

Au (g/t) |

Ag (g/t) |

Cu (%) |

Pb (%) |

Zn (%) |

Au (koz) |

Ag (koz) |

Cu (kt) |

Pb (kt) |

Zn (kt) |

|||||||||||||||||||||||

| 0 | 2,553 | 3.2 | 39.8 | 2.5 | 0.5 | 3.5 | 263 | 3,264 | 65 | 13 | 90 | |||||||||||||||||||||||

| 1 | 2,528 | 3.2 | 40.1 | 2.6 | 0.5 | 3.6 | 263 | 3,262 | 65 | 13 | 90 | |||||||||||||||||||||||

| 2 | 2,373 | 3.4 | 42.4 | 2.7 | 0.5 | 3.8 | 260 | 3,238 | 64 | 13 | 89 | |||||||||||||||||||||||

| 3 | 2,055 | 3.8 | 46.9 | 3.0 | 0.6 | 4.2 | 251 | 3,097 | 62 | 12 | 87 | |||||||||||||||||||||||

| 4 | 1,846 | 4.1 | 50.0 | 3.3 | 0.6 | 4.6 | 244 | 2,966 | 61 | 12 | 84 | |||||||||||||||||||||||

| 5 | 1,655 | 4.4 | 53.7 | 3.5 | 0.7 | 4.9 | 236 | 2,860 | 59 | 11 | 80 | |||||||||||||||||||||||

| 6 | 1,461 | 4.8 | 58.5 | 3.8 | 0.7 | 5.2 | 225 | 2,747 | 56 | 11 | 75 | |||||||||||||||||||||||

| 7 | 1,320 | 5.1 | 62.4 | 4.1 | 0.8 | 5.5 | 217 | 2,647 | 54 | 10 | 72 | |||||||||||||||||||||||

| 8 | 1,195 | 5.4 | 66.0 | 4.3 | 0.8 | 5.8 | 208 | 2,535 | 51 | 10 | 69 | |||||||||||||||||||||||

| 9 | 1,111 | 5.7 | 68.6 | 4.4 | 0.9 | 5.9 | 202 | 2,449 | 49 | 10 | 66 | |||||||||||||||||||||||

| 10 | 1,019 | 5.9 | 71.4 | 4.6 | 0.9 | 6.1 | 194 | 2,340 | 47 | 9 | 63 | |||||||||||||||||||||||

Updated Mineral Resources Estimate Notes:

- This Updated Mineral Resources Estimate as of March 30, 2019 was prepared in accordance with NI 43-101 and CIM Standards (2014).

- The Updated Mineral Resource Estimate tonnages have been rounded to the nearest 10,000 and AuEq, Au, Ag, Cu, Pb and Zn grades have been rounded to one decimal. Troy ounces have been rounded to kilo troy ounces (koz), and tonnes of Cu, Pb, and Zn have been rounded to kilo-tonnes (kt).

- The Updated Mineral Resources Estimate for the La Mina VMS polymetallic deposit have been classified as Inferred Mineral Resources.

-

The Updated Mineral Resources has been reported at various cut-off

grades to demonstrate the grade-tonnage relationship. The preferred

reporting cut-off grade is 4 g AuEq / t (4 gold equivalent grams /

tonne) based on an in-situ gross value of $165 per tonne. The AuEq / t

formula is:

AuEq ppm = Au ppm + (Cu % * 1.454) + (Ag ppm * 0.013) + (Zn % * 0.654) + (Pb %*0.532) - The Updated Mineral Resources could be accessed by developing a mine ramp and are considered reasonable prospects for economic extraction in the foreseeable future.

-

The Updated Mineral Resources Estimate is based on the following three

year trailing monthly average prices of metal, as of January 31st,

2019:

$1,264/ troy oz Au

$2.68/lb Cu - $5,909 / t Cu

$1.21/lb Zn - $2,656 / t Zn

$16.64/ troy oz Ag

$0.98/lb Pb – $2,162 / t Pb - This Updated Mineral Resources Estimate was prepared by Brian R. Wolfe, BSc (Hons), MAIG.

- Mineral Resources do not have demonstrated economic viability.

- This Updated Mineral Resources Estimate may be materially affected by environmental, permitting, legal title, taxation, socio-political, marketing or other relevant issues.

QA/QC Statement

Toachi implemented a concise QA/QC program for all their drill hole assay data. Toachi completed a total of 80 diamond drill holes for a total of 13,747 m between August 2016 and July 2017 under the supervision of the project manager for Toachi. The drill holes were drilled using diamond drill technique, with 12,557m HTW diameter core (71.0mm), with 1,137m of NTW (56.2mm) and 53m of BTW (42.1mm) diameter. Toachi implemented a strict QA/QC regiment related to all aspect of core handling, sampling and logging.

Both labs (ALS and MSA) also completed their own internal checks. This data, along with the Toachi Mining checks was validated using QCAssure software. Toachi Mining also conducted additional QA/QC checks on all their data by submitting approximately 7% of their drilling database to an independent laboratory. Samples selected covered the top 200 assay values, then a mix of different assay values throughout each original lab job returned.

PEA Metallurgy

Four composite samples representing the expected zones of the ‘La Mina’ VMS deposit mineralized horizons have been tested at SGS Lakefield. Following a program of some 55 Rougher/Scavenger and bulk cleaner tests, the results show that the La Mina VMS deposit polymetallic mineralization responded well to a conventional flotation flowsheet and produced saleable grade concentrates. Locked cycle tests (LCT-1) were conducted on the composite sample of zone 300 with primary grinding at P80 = 65 microns, copper and zinc regrinds at P80 = 20 microns. The PEA is based on LCT-1 test results.

The flotation test work showed good metal recoveries, creating saleable Copper-Lead and Zinc concentrates. Copper-Lead concentrate showed the following grades and recoveries:

| Copper-Lead Concentrate | Grade | Recovery | |||||||||

| Cu | 20 -23 % | 88 - 90 % | |||||||||

| Pb | 4 - 5 % | 70 - 72% | |||||||||

| Au | 10 - 13 g/t | 41 - 43 % | |||||||||

| Ag | 140 - 145 g/t | 45 - 50 % | |||||||||

Zinc concentrate showed the following grades and recoveries:

| Zinc Concentrate | Grade | Recovery | |||||||||

| Zn | 50 - 52% | 70 - 72% | |||||||||

| Au | 11 - 13 g/t | 25 - 27 % | |||||||||

| Ag | 114 - 125 g/t | 25 - 27 % | |||||||||

Figure 2 summarizes the results of the Locked Cycle Test LCT-1.

The results from LCT-1 form the basis for the concentrator preliminary design. Further metallurgical work can optimize the process and test the benefit of adding a gravity circuit and pyrite recovery on zinc flotation tailings.

Metallurgical test work was conducted by SGS Canada Inc. in Lakefield, Ontario, Canada, under the direct supervision of Dan Imeson, Manager, Mineral Processing. Dan Imeson has over 20 years of experience in the mineral processing field with SGS Canada.

PEA Mining Plan

For mine planning purposes, the La Mina VMS deposit North block was subdivided into two zones referred to as the “Upper North zone” and the “Lower North zone”. The Upper North Zone and the Lower North zone are scheduled to be mined between Years 1 to 3 and Years 2 to 8 respectively. The La Mina VMS deposit South block, referred to as the “South zone” is scheduled to be mined in Years 3 to 8. A ramp is developed to access the Upper North zone, and another ramp is developed to access the Lower North zone and the South zone. Deepest workings are approximately 350 metres below surface.

The Upper North zone and Lower North zone are mined using the drift and slash with cemented rock fill (CRF) backfill method – a variant of cut and fill mining. A 33 m high stope panel as an example would be developed in 3 m high lifts and accessed by two access ramps: an access decline serving the lower section of the stope; and another ramp to access the lifts in the upper section of the stope. The backs of an access ramp would be slashed after a lift is backfilled in order to maintain access to the next lift. Each lift would be developed by driving a 3 m high x 4 m wide pilot drift in mineralization along strike, and then slashing the mineralization on the footwall and hangingwall sides of the pilot drift to the shanty wall stope limits. In areas where the mineralization pinches, the pilot drift is widened to maintain a minimum 4 m mining width. The proposed stope development sequence including ground support and CRF backfill were selected based on the mineralization, footwall and hangingwall characteristics and geometry and geotechnical factors. The back and walls are supported using pattern bolting and welded wire mesh. Once mined, each lift would be backfilled using CRF.

Most lifts would be mined in an overhand manner. The cement content of CRF placed in lifts that are scheduled to be under-mined by another lift is increased to 8 wt%. The drift and slash with CRF backfill method is also used to mine the majority of the stopes in the South zone. The uppermost part of the South zone is mined using room and pillar stopes with CRF backfill. Primary cut and fill stopes are developed by driving 4.5 m high x 4.5 m wide drifts transversely in mineralization and then CRF backfilling them. Secondary cut and fill stopes are then developed between the primary stopes. The ground support in the room and pillar stopes includes cable bolts, pattern bolting, welded wire mesh and shotcrete.

The break-even cut-off grade expressed in gold equivalent grams per tonne milled terms is 4.24 g Au Eq / t milled. It represents the gold equivalent grade of recovered diluted polymetallic mine material where the revenue generated by mining and processing a tonne of the material equals the costs incurred in producing that revenue.

The mine development and stoping sequence was selected to reduce upfront mine development time lines and cost; make a sufficient number of stope faces available for stoping / backfilling over the mine life; and to provide a flexible approach. The mine schedule is shown in Figure 3.

PEA Processing Plant and Infrastructure

The following describes the process flow sheet for an 800 tonnes per day copper, lead, zinc, gold and silver mineral processing facility.

The crushing plant would process the run-of-mine (ROM) material by using a primary jaw crusher to reduce the material from a nominal 18 inches to a 100% passing (P100) of 249 mm (P80 of 114 mm). The grinding circuit is a semi-autogenous (SAG) mill - ball mill grinding circuit with subsequent processing in a flotation circuit. The SAG mill operates in closed circuit with a vibrating screen. The ball mill operates in closed circuit with hydrocyclones.

Cyclone overflow, the grinding circuit product, is fed to the flotation plant. The flotation plant consists of copper/lead and zinc flotation circuits. The copper/lead flotation circuit consists of rougher flotation and three-stage cleaner flotation. The zinc flotation circuit consists of rougher flotation and two-stage cleaner flotation.

Both copper/lead and zinc concentrates are thickened, filtered, and stored in concentrate storage facilities prior to loading onto trucks for shipment. Zinc rougher flotation tailing and zinc first cleaner scavenger tailing are the final tailing. Tailing thickener underflow is pumped to a tailings storage facility (TSF). Plant water stream types include copper/lead process water, zinc process water, fresh water, and potable water.

The overall flowsheet is shown in Figure 4.

PEA Infrastructure

A power line would be constructed from the national grid to a substation adjacent to the mill. An administration building would be installed along with a mine office, health and safety, training centre and change rooms complex. A shop / warehouse, CRF plant and ancillary services and buildings would be constructed to service the mine. The main mine ventilation fans would be installed on surface. Explosive and detonators would be stored in secure magazines located inside the mine. Tailing are placed in an engineered TSF.

PEA Product Marketing

The NSR information used in the PEA was developed following a review of publicly available NSR information including NI 43-101 reports and other public disclosures and information received from metal concentrate traders. The NSR terms are based on information received on or before March 30th, 2019. The PEA assumes that the Cu / Pb concentrate and the Zn concentrate would be exported and sold to smelters in Asia. Metallurgical test results show the concentrates are marketable.

PEA Environmental and Social Environmental aspects:

No significant adverse environmental impact is foreseen. The conceptual level Project encompasses environmental protection technologies. The mill products (Cu/Pb and Zn concentrates) are exported for treatment. Mine waste rock is used to produce CRF backfill. Clean non-acid producing waste rock is imported to produce CRF when there is insufficient mine waste rock available. Water from the mine and the TSF is collected and treated prior to its recycle or release. The mill and mine process water are obtained from the mine, water treatment plant and on-site wells. Potable water is obtained from a well. The Project includes sewage collection and treatment systems, double wall fuel storage tanks, and spill kits as examples. The Company would also have procedures to help it avoid producing hazardous wastes where possible and used batteries or waste chemicals are properly disposed of using licensed contractors. The Company’s environmental staff would monitor and report on the environmental performance of the Project.

The Project is closed and rehabilitated at the end of the mine life. The closure works include the removal of un-used chemicals from the mill, mill demolition, the removal of equipment and consumables from the mine, the sealing of mine openings, the removal and proper disposal of unused fuel, lubricants and chemicals, infrastructure demolition, and the construction of an engineered cap over the TSF. The effectiveness of the closure works would be evaluated using a monitoring program.

Community consultation:

Ecuador has an established regulatory framework for social and environmental assessment and mine permitting. The country is encouraging and is open to mining sector investments as indicated by the recent level of interest and investment in its mining sector. It is widely recognized that obtaining social community approval has proven challenging for some other mining projects in the country. Toachi has fortunately been proactive in this area as its Social Consultation Director has informed local people about the Company’s vision. The Company reports that it has local public support for a project with few dissenters, and that it plans to continue to consult with local people and others who could be potentially impacted by the Project. Census results indicate that Indigenous persons account for 1% of the local Palo Quemado township population. Recent official decisions including a decision to cancel a referendum on another mine project in Ecuador indicate the regulatory regime for mining is functioning.

Outlook:

The legal framework to license, develop and operate the Project is in place. The Company’s success in this regard appears to largely depend on the success of its future community social consultation efforts. Delays in project permitting and implementation may occur.

The Project requires that Toachi obtain a concession registration for the property as a medium scale (301-1,000 tpd throughput) mining property. It is currently a registered as a small scale (up to 300 tpd throughout) mining property.

The Project has been designed to a conceptual level and may be revised and improved. The PEA makes use of Inferred Resources which are not mineral reserves and there is no guarantee that the Project described in this PEA can be implemented.

Risk and Opportunity

Key potential risks:

- The Project could be materially affected by social, political, environmental, permitting, legal title, taxation, marketing and other relevant issues.

- The costs for acquiring surface access / surface land rights from local landowners are not known with confidence at this point and are not included in the PEA, and the time line to obtain them could delay the Project.

- Obtaining community social approval for permitting, development and operations appears to be a crucial aspect for the Project. There is a risk that the Company’s community engagement program may need to be bolstered to maintain wide local support for the Project. There is a latent risk of project delays.

Key opportunities for improvement:

- The metallurgical testing completed to date indicates that it may be possible to increase gold recovery to the Cu/Pb concentrate which offers higher payables for gold by initial grinding to 20 microns.

- It may be possible to optimize the mine development and stoping sequence to improve the run of mine grade to the mill in the initial years of the Project and improve the project economics.

- The recommended technical studies may lead to productivity improvements, mine operating cost savings and/or improved environmental protection.

- The recommended study into the use of battery-powered mine and surface haulage equipment could lead the use of this equipment and provide an opportunity to reduce mine ventilation power costs.

PEA Key Recommendations

Key recommendations are summarized below along with estimated costs.

| Recommendation | Estimated cost | |||

| Conduct a surface diamond drilling program to convert where possible Inferred Mineral Resources to the Indicated Mineral Resources and/or Measured Mineral Resources categories and explore a possible deeper extension of the La Mina VMS deposit South block. 15,900 m @ $250/m | $4,000k | |||

| Conduct a mine geotechnical characterization and design study. | $240k | |||

| Conduct a tailings / waste rock storage options study. Possible options are to: use cemented and uncemented rock fill in stopes; use cemented paste to backfill stopes; co-dispose waste rock and hydraulic/filtered/paste tailings in a TSF; and combinations of the above. | $400k | |||

| Conduct a hydrological / hydrogeological study to evaluate the mill water balance and process water supply options, and TSF water pond storage and final effluent treatment plant capacity requirements. | $250k | |||

| Carry out a study to expand the Company’s socio-economic baseline. | $250k | |||

| Conduct additional metallurgical testwork to optimize metal recoveries, concentrate grades and mill process. | $250k | |||

| Total cost to implement key recommendations | $5,390k | |||

Qualified Persons and NI 43-101 Disclosure

Independent Qualified Person David Orava, P.Eng. of SGS Geological Services / Services Géologiques SGS, has supervised the preparation, prepared, revised and approved the technical contents of this news release.

This PEA is preliminary in nature and includes Inferred Mineral Resources that are too speculative geologically to have economic considerations applied to them to be categorized as Mineral Reserves. Mineral Resources are not Mineral Reserves and do not have demonstrated economic viability.

About Toachi Mining Inc.

Toachi brings a disciplined and veteran team of project managers together with one of the industry’s highest grade polymetallic projects at the La Mina VMS deposit in Ecuador. Toachi is focused on and committed to the development of advanced stage mineral projects throughout the Americas using industry best practices combined with a strong social license from local communities. Toachi Mining has 81,166,435 shares issued and outstanding.

Forward Looking Statements

Certain statements contained in this news release may constitute “forward-looking information” as such term is used in applicable Canadian securities laws. Forward-looking information is based on plans, expectations and estimates of management at the date the information is provided and is subject to certain factors and assumptions, including, that the Company’s financial condition and development plans do not change as a result of unforeseen events and that the Company obtains regulatory approval. Forward-looking information is subject to a variety of risks and uncertainties and other factors that could cause plans, estimates and actual results to vary materially from those projected in such forward-looking information. Factors that could cause the forward-looking information in this news release to change or to be inaccurate include, but are not limited to, the risk that any of the assumptions referred to prove not to be valid or reliable, that occurrences such as those referred to above are realized and result in delays, or cessation in planned work, that the Company’s financial condition and development plans change, and delays in regulatory approval, as well as the other risks and uncertainties applicable to the Company as set forth in the Company’s continuous disclosure filings filed under the Company’s profile at www.sedar.com. The Company undertakes no obligation to update these forward-looking statements, other than as required by applicable law.

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

View source version on businesswire.com: https://www.businesswire.com/news/home/20190430005522/en/